Introduction

The Colorado General Assembly is currently working to finalize the 2024-25 state budget, which would take effect July 1.

As in other sessions, lawmakers in 2024 say they have shortfalls, butting heads with TABOR restrictions while fighting for increased funding for workforce housing, higher education, and healthcare reimbursement. The public framing is the same: “The state does not have enough money.”

CSI’s findings, however, do not show Colorado as a cash-strapped state. Revenue grew 70% between 2011 and 2021, much of it from fees that skirt TABOR’s revenue caps, and its debt level rose 35%. The size and scope of government employment should give a good idea of the trend. There are 42,000 more government employees in 2021 than in 2011.

The state does not hoard this revenue. Even though its spending as a share of GDP dropped, it still ranks in the top ten for spending as share of GDP – meaning other states have tightened their spending further.

“Shortfall” gives the incorrect impression. The state may have less a revenue problem than a spending problem.

Key Findings

- While Colorado ranks lower on state and local government employment as a percentage of population and debt service as a share of tax revenue, it ranks in the top 10 of state and local government spending as a percentage of GDP.

- Colorado ranks 38th in the nation regarding its government budget competitiveness.

- Since 2017, Colorado’s competitiveness in this area compared has decreased and is now comparable to levels of the early 2010s.

- Colorado’s Government Budget Competitiveness Index decreased slightly from 71 to 70 from 2011 through 2023. It fell from a peak of 75 in 2018.

- Government revenue from taxes, fees, and miscellaneous sources increased 63.9% from $32.3 billion in 2011 to $52.9 billion in 2021. Comparatively, the population has increased 13.6% and GDP has increased 63.1%.

- Government spending as a percentage of GDP decreased from 18.5% in 2011 to 16.4% in 2023.

- Government debt increased 35.1% from $51.6 billion in 2011 to $69.8 billion in 2023.

- Government Debt Service as a Percentage of Tax Revenue Competitive Index increased from 51 to 54.

- The share of debt outstanding remained constant at 32% from state government debt and 68% from local government debt.

- Healthcare and education consume 69.4% of the total state government budget.

Colorado’s Free Enterprise Report and State Budget Competitiveness

CSI issues a Free Enterprise Report annually. The report assesses the state’s competitiveness relative to 49 other states and the District of Columbia and provides data and analysis on eight policy areas: education, energy, healthcare, housing, infrastructure, public safety, budget, and taxes and fees. This report is intended to provide additional detail on the budget competitiveness not covered in the Free Enterprise Report.

The competitiveness indices should be interpreted as follows: an increase (decrease) in an index indicates increased (decreased) competitiveness relative to the other 49 states and the District of Columbia. Colorado’s individual performance may improve, for instance government spending as a percentage of GDP may decrease, however, other states may have seen greater decreases. This would cause Colorado’s competitiveness in government spending as a percentage of GDP to decline.

Government Budget Competitiveness Index

As James Madison explained in The Federalist,

“The powers delegated by the proposed Constitution to the federal government are few and defined…. [T]he powers reserved to the several States will extend to all the objects which, in the ordinary course of affairs, concern the lives, liberties, and properties of the people, and the internal order, improvement, and prosperity of the State.” These reserved powers have generally been referred to as “police powers,” such as those required for public safety, health, and welfare.

For states to fulfill the reserved powers, they collect revenue from a variety of sources, taxes, debt, and develop budgets that allocate resources towards the fulfillment of the various police powers.

To gauge how well states are performing regarding sound budgeting and fiscal restraint, CSI produces a Government Budget Competitiveness Index for all 50 states and the District of Columbia consisting of three metrics:

- The debt service as a percentage of tax revenue

- Government employment as a percentage of the state’s population

- Government spending as a percentage of state GDP

Each metric is ranked relative to all 50 states and the District of Columbia. Then the three ranked metrics are equally weighted and summed. This value is ranked again to produce an aggregate measure of state budget competitiveness as shown in

Figure 1. Colorado’s Government Budget Competitiveness was 71 in 2011, peaked in 2018 at 75, and then fell to 70 in 2023.

Figure 2 shows the evolution of the three-component metrics that are included in the Government Budget Competitiveness Index. The Government Spending as a Percentage of GDP Index rose from 85 in 2011 to 93 in 2023. It peaked in 2018 and 2019 at 94. The Government Employment as a Percentage of Population Index dropped from 77 in 2011 to 62 in 2023. The Government Debt Service as a Percentage of Tax Revenue Index increased slightly from 51 in 2011 to 54 in 2023.

Government Debt, Tax and Fee Revenue

State governments may have limitations on budgets. In 2021 the National Association of State Budget Officers (NASBO) published the figures on the number of states that have limitations on state budgets by type of limit. Figure 3 shows the published figures in NASBO’s 2021 report titled, “Budget Processes in the States 2021.”

Forty-nine states have balanced budget amendments, 43 have limits on debt and debt service, 26 have limits on tax and expenditure, and 10 have appropriation limits.

Figure 3

The Colorado Constitution requires the state to balance its budget annually. Each year, the Colorado General Assembly must pass a budget and each budget must be balanced but it can carry a deficit into the next year. The Colorado state government cannot spend in excess of the tax and fee revenue that it actually collects or saves.

Article X, Section 20 of the Colorado Constitution, or TABOR was added to the state constitution by a vote of the people in 1992. TABOR limits the amount of increase in state government spending from one fiscal year to the next. That way, if state revenues increase sharply during a given year, the state government is further limited as to how much of that increase it can use in the next fiscal year budget. Under TABOR, state fiscal year spending can increase no more than the rate of inflation, plus the percentage change in state population during the prior calendar year, adjusted for revenue changes approved by voters after 1991.

TABOR also removed the power from the state legislature to create a new tax or to increase the rate of an existing tax. Under TABOR, a proposal to create a new tax or to increase the rate of an existing tax must be directed to Colorado voters.

Colorado also limits spending. A constitutional formula calculates the state spending limit by multiplying a base amount by inflation and population growth. The base amount is the lesser of the prior year’s revenue or spending limit. The formula adds voter-approved revenue changes into the limit calculation. In practice, the limit on state fiscal year spending functions as a limit on the amount of revenue the state can collect and retain from certain sources, because revenue is subject to the limit regardless of whether it is spent or saved. Revenue in excess of the limit must be refunded to the taxpayers.[i] Both the revenue and spending rules are binding and thus a legislative supermajority or vote of the people is required to override them. On top of these rules, the state limits both its authorized debt and debt service.

Colorado state and local governments can issue debt. However, there are specific laws governing public debt. The law governing public debt is contained in Article XI of the Colorado Constitution.[ii] There are many ways in which state and local governments can borrow money, for example general obligation bonds, revenue anticipation notes, or certificates of participation.[iii]

- General Obligation Bonds: Colorado's Constitution prohibits the state from borrowing money with a general promise to repay. These bonds, called general obligation bonds, are guaranteed largely by the taxing authority of the government. Local governments in Colorado can issue general obligation bonds with voter approval. For example, Colorado school districts, if they receive the approval of their voters, can issue general obligation bonds to build or renovate schools. These bonds are repaid from school district property taxes.

- Tax or Revenue Anticipation Notes: Tax revenue anticipation notes represent money borrowed by a government on the pledge that it will be repaid over time from a specified revenue source. The Treasurer's Office issues tax revenue anticipation notes to help the annual cash flow needs of the state's General Fund or that of local school districts. Those notes are repaid within the same fiscal year (or repayment resources are placed in escrow). The state's constitution prohibits multi-year fiscal obligations without voter approval, which includes tax revenue anticipation notes with a repayment period longer than a year (except those issued by government-run businesses, called enterprises). The voters of Colorado approved the issuance of transportation revenue anticipation notes for the construction of highway projects in 1999.

- Certificates of Participation: A lease-financing mechanism where the government enters into an agreement to make regular lease payments for the use of an asset over some period, after which the title for the asset transfers to the government. Since the government can decide, at any time, to discontinue the lease, COPs do not constitute a multi-year fiscal obligation and so can be issued without voter approval.

Colorado’s government spending at any point in time can be financed with taxes or by selling more debt. In the case of debt issuance, the government collects real resources via voluntary transactions with economic agents who are willing to trade real resources today for the promise of real resources in the future. Debt buyers, including households saving for retirement, view this debt as savings, which reduces their savings in private investment. This substitution to public debt from private debt is called the “capital crowding-out effect” from government debt issuance. State saving, therefore, is reduced more when the new government debt is used to finance more immediate consumption (e.g., social transfers) compared to longer-term public investment (e.g., roads and pre-K education). The types of debt issued by the State of Colorado can be found at the Colorado Department of Treasury website.

[iv]

Because of the crowding out effect on the free enterprise system, CSI chose to include metrics that capture state and local governments revenue and debt over time to measure the amount of taxation and debt issuance from the state and local governments. CSI does not have data on private investment funded with debt, but data is available on public debt for state and local government from the U.S. Census, Annual Survey of State and Local Finances (latest available is 2021, released in August 2023). Figure 4 - shows revenue from taxes, charges, and miscellaneous revenue for state and local government in Colorado, excluding federal sources. Additionally, it shows state and local government public debt.

Figure 4

|

Colorado State & Local Government Revenue, Debt, Spending, and State GDP.

|

|

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

% change 2011-2021 |

| Revenue |

| State Government Tax Revenue |

$9.5B |

$10.3B |

$11.3B |

$11.8B |

$12.7B |

$12.9B |

$13.3B |

$14.9B |

$15.9B |

$15.1B |

$18.8B |

98.8% |

| Local Government Tax Revenue |

$10.9B |

$10.9B |

$11.2B |

$11.6B |

$11.9B |

$12.8B |

$14.1B |

$14.6B |

$16.2B |

$17.5B |

$18.4B |

68.5% |

| State Government Revenue from Charges & Misc. Revenue |

$5.4B |

$5.1B |

$5.3B |

$5.6B |

$5.5B |

$5.7B |

$6.0B |

$6.8B |

$7.0B |

$7.0B |

$6.9B |

27.6% |

| Local Government Revenue from Charges & Misc. Revenue |

$6.5B |

$6.8B |

$7.2B |

$7.2B |

$7.0B |

$7.4B |

$8.3B |

$8.3B |

$9.2B |

$9.6B |

$8.8B |

35.7% |

| State Government Revenue from Taxes and Charges & Misc. Revenue |

$14.9B |

$15.4B |

$16.5B |

$17.3B |

$18.3B |

$18.6B |

$19.4B |

$21.8B |

$22.9B |

$22.1B |

$25.7B |

72.9% |

| Local Government Revenue from Taxes and Charges & Misc. Revenue |

$17.4B |

$17.7B |

$18.4B |

$18.8B |

$18.9B |

$20.2B |

$22.4B |

$22.9B |

$25.4B |

$27.2B |

$27.2B |

56.3% |

| Total State and Local Revenue from Taxes and Charges & Misc. Revenue |

$32.3B |

$33.1B |

$34.9B |

$36.1B |

$37.2B |

$38.8B |

$41.7B |

$44.6B |

$48.3B |

$49.3B |

$52.9B |

63.9% |

| State Government Share of Revenue from Taxes and Charges & Misc. |

46.0% |

46.5% |

47.3% |

48.0% |

49.1% |

47.9% |

46.5% |

48.8% |

47.4% |

44.9% |

48.6% |

|

| Local Government Share of Revenue from Taxes and Charges & Misc. |

54.0% |

53.5% |

52.7% |

52.0% |

50.9% |

52.1% |

53.5% |

51.2% |

52.6% |

55.1% |

51.4% |

|

| Debt |

| State Government Debt Outstanding |

$16.3B |

$16.1B |

$16.4B |

$16.4B |

$16.9B |

$16.8B |

$17.0B |

$17.9B |

$18.7B |

$20.2B |

$22.3B |

36.7% |

| Local Government Debt Outstanding |

$35.3B |

$35.4B |

$37.1B |

$37.9B |

$39.0B |

$37.3B |

$40.3B |

$38.5B |

$45.4B |

$46.5B |

$47.4B |

34.4% |

| State & Local Government Debt Outstanding |

$51.6B |

$51.5B |

$53.5B |

$54.3B |

$55.9B |

$54.0B |

$57.3B |

$56.3B |

$64.1B |

$66.7B |

$69.8B |

35.1% |

| State Government Share of Debt Outstanding |

31.6% |

31.2% |

30.6% |

30.1% |

30.3% |

31.0% |

29.6% |

31.7% |

29.2% |

30.2% |

32.0% |

|

| Local Government Share of Debt Outstanding |

68.4% |

68.8% |

69.4% |

69.9% |

69.7% |

69.0% |

70.4% |

68.3% |

70.8% |

69.8% |

68.0% |

|

| GDP |

| Colorado GDP |

$268B |

$277B |

$292B |

$310B |

$321B |

$330B |

$349B |

$372B |

$395B |

$391B |

$436B |

63.1% |

| Spending |

| State & Local Government Direct Expenditures |

$49.6B |

$49.7B |

$50.5B |

$53.7B |

$55.2B |

$57.9B |

$60.9B |

$64.5B |

$66.7B |

$74.1B |

$79.3B |

59.7% |

Government tax revenue has doubled since 2011 and in 2021 was $18.8 billion. Local government tax revenue increased 68.5% from $10.9 billion in 2011 to $18.4 billion in 2021. The state government has been circumventing TABOR by raising revenue from fees and as such are not subject to the limitations imposed by TABOR. State government revenue from fees (charges) and miscellaneous revenue rose 27.6% from $5.4 billion in 2011 to $6.9 billion in 2021. Local governments increased revenues from fees (charges) and miscellaneous revenue by 35.7% from $6.5 billion in 2011 to $8.8 billion in 2021.

Total state and local government revenue from taxes, fees, and miscellaneous revenue rose 63.9% from $32.3 billion in 2011 to $52.9 billion in 2021. This is in line with nominal growth of GDP by 63% from $268 billion in 2011 to $463 billion in 2021.

Public debt issued from state and local governments grew 35.1% from $51.6 billion in 2011 to $69 billion in 2021. The share of public debt between state government and local governments has remained constant between 2011 and 2021 at 32% from the state government and 68% from local governments.

Colorado ranks 12

th in the amount of outstanding public debt in 2021 among all fifty states and the District of Columbia. By comparison, California ranks 1

st with $541.2 billion, and Wyoming ranks 51

st with $2 billion.

Government Debt Service as a Percentage of Tax Revenue

Figure 5

Government Employment as a Percentage of Population

Figure 6

CSI chose the percentage of government employment as a percentage of the population as a measure of government encroachment. Figure 6 shows the competitiveness index and government employment as a percentage of the population. The competitiveness index declined from 77 in 2011 to 62 in 2023. Most of the decline began after 2018.

Government employment as percentage of population increased marginally from 5.27% in 2011 to 5.34% in 2023.

Government Spending as a Percentage of GDP

Figure 7

Government Spending as a Percentage of GDP Competitive Index rose from 85 in 2011 to 93 in 2023. This improvement is due in large part because government spending as percentage of GDP fell from 18.5% in 2011 to 16.4% in 2023.

Colorado ranks 6th in the percentage change in GDP from 2011 through 2023 at 63.1%. This has been the primary driver behind the increase in this competitiveness metric. By comparison, Utah ranks 1st in GDP growth with 79.5%, and Alaska ranks 51st with the lowest increase in GDP at 0.8%.

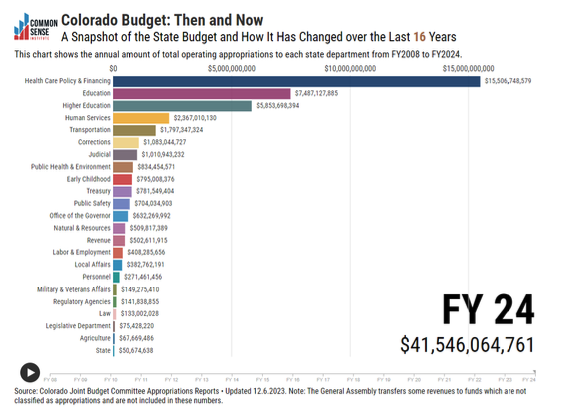

Figure 8 shows the composition of the government budget spending in FY 2024. Spending is dominated by health care policy and financing consuming $15.5 billion, 37.3% of the total budget of $41.6 billion. The second largest spending is on education at $7.5 billion (18% of budget), followed by higher education $5.9 billion (14.1% of budget). These three-line items account for 69.4% of the total budget. By comparison, in 2011 they accounted for 61.7% of the total budget. With spending on healthcare and education (K-12 and higher education) consuming an increasing share of the budget, other spending priorities come under increasing pressure.

Going Forward

Government revenue has outpaced inflation and population growth in recent years, and state and local spending is continually adding new spending on homeless and migrant programs with little impact on curbing the growth of either population. Additionally, government employment has increased 15.5% (41,829 jobs) since 2011, more than the 13.6% increase in the population and can be expected to increase more as new regulatory programs are introduced.

Failure to manage public sector spending and debt issuance in a fiscally responsible manner will erode Colorado’s competitiveness relative to other states. Other states that have failed to be fiscally responsible have experienced massive out-migration, reducing the tax base putting further pressure on state.

Source and Notes

[i] Colorado Legislative Council Staff Issue Brief, number 15-14, September 2015

[ii] https://leg.colorado.gov/colorado-constitution

[iii] Treasury.colorado.gov/public-finance-debt-issuance.

[iv] https://treasury.colorado.gov/overview-of-debt-and-official-statements