Introduction

Last week, the economy and markets experienced a short-lived but substantial scare. On Friday, August 2

nd, the United States Bureau of Labor Statistics (BLS) released new employment data showing the U.S. added 35% fewer jobs in July than anticipated, signaling a potential weaking of the labor market. In addition, unemployment rose to 4.3%—the highest since October 2021. The S&P500 fell 1.8% that day. Trouble in the Japanese treasury market early Monday morning caused a cascade of forced selling of global equities, with the S&P500 falling an additional 3% on Monday. This week’s inflation print and state-level employment data eased concerns for now, and markets have since recovered. Nonetheless, last week’s events have elevated concerns over an economic slowdown.

Various economic indicators, actions by the Federal Reserve, and updated jobs and inflation numbers can all help understand where the economy is headed next. Historically, whenever the United States falls into a recession, Iowa follows soon thereafter. Iowans will need to pay attention to state and national policies and data trends for warnings signs of what lies over the horizon for the state’s economy. Therefore, this month’s CSI inflation and jobs report will consider both state and national trends to assess the health of Iowa’s economy and possible leading indicators of weakness.

Key Findings

- July’s jobs and inflation print bring concern about an economic slowdown but give investors hope that the Fed will ease monetary conditions.

- An increase in inflation and falling employment in Iowa suggests a decline in economic conditions, though still stronger than the broader U.S.

- The U.S. unemployment rate rose from 4.1% to 4.3%, triggering the Sahm Rule, a leading economic indicator of recession.

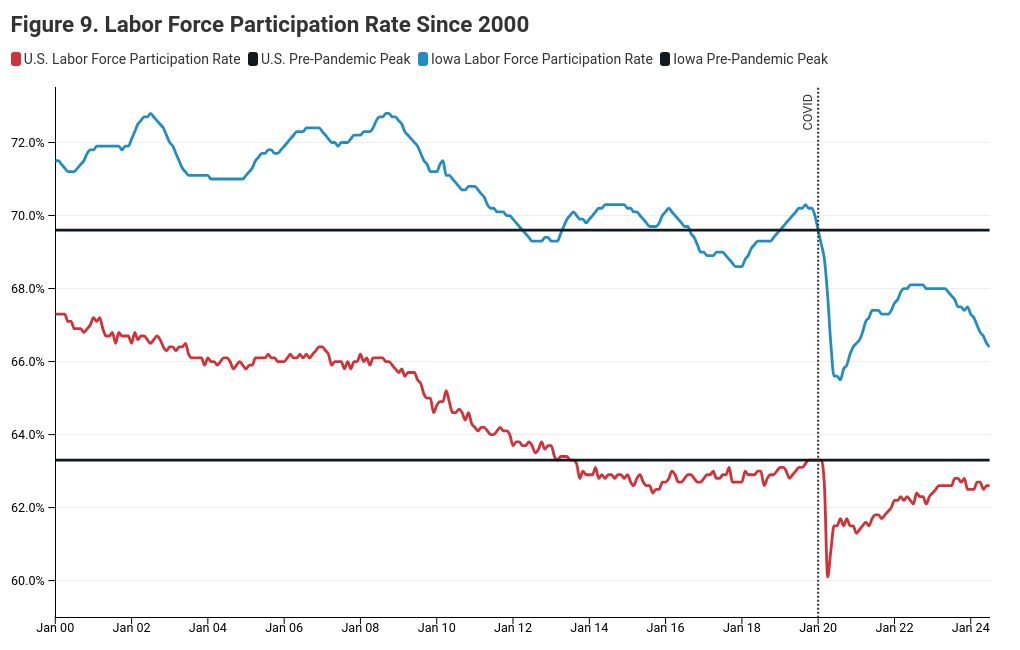

- While Iowa’s unemployment rate remains low at 2.8%—7th lowest in the nation—its labor force participation rate continues to decline.

- Iowa’s LFPR (labor force participation rate) fell from June to July by 0.1 percentage points to 66.4%. This continues Iowa’s LFPR decline, which started in May 2023. The United States has not experienced a similar trend.

- Contrary to what the unemployment rate suggests, the U.S. is gaining employment while Iowa employment is falling.

- According to the household survey, Iowa lost 1,500 jobs in July—wiping all gains since February 2024. The establishment survey reported 3,565 fewer jobs.

- As Iowa lost jobs, the United States gained 94,600, according to the establishment survey.

- In July, inflation in the U.S. fell from 3% to 2.9%, its lowest point since March 2021. Inflation in Iowa rose from 2.5% to 2.7%.

- Since the pandemic, prices in the Midwest have risen a total of 22.2% versus 21.86% for the U.S.

- The average household has spent a total of $28,980.48 more since 2020 because of higher inflation. In July, the average midwestern household spent over $1,000 more due to inflation relative to 2020.

- In the Midwest region from July 2023 to July 2024, the price of fuels and utilities grew by 5.9% and the price of housing grew by 5.88% while the price of durables fell by 4.8%.

Will the economy experience a soft landing?

Economists, the Federal Reserve, investors, and others attempting to gauge the health of the economy monitor various economic indicators. A non-partisan research organization dedicated to the protection and promotion of Iowa’s economy, Common Sense Institute publishes reports each month breaking down and analyzing new government inflation and employment data. These data directly impact Iowa families, businesses, and workers. The typical Iowa household today must spend over $1,000 more per month than in 2020 to maintain the same standard of living. A sharp rise in unemployment would bring even more hardship. Therefore, those in control of monetary and fiscal policy at the national level also closely monitor inflation and employment data to inform their policy decisions. Indeed, federal law requires the Federal Reserve (the Fed) to pursue monetary policies that ensure stable prices and maximum employment as their so-called “dual mandate.”

[i]

The Fed governs U.S. monetary policy by controlling the federal funds rate and by purchasing assets such as U.S. Treasury bonds and mortgage-backed securities on the open market. These actions impact the cost of borrowing, directly or indirectly impacting mortgage and loan rates, savings account yields, inflation, consumer spending, and business investments. Thus, the Fed closely monitors BLS inflation and employment data to determine monetary policy in service of their congressional mandate. Put simply, monetary policies at the national level can have a tremendous impact on Iowa’s economy and on the wellbeing of Iowans.

The central bank interprets its mandate of stable prices as a directive to keep inflation at 2%. When inflation surged to a 40-year record high of 8.2% in March 2022, the Fed began to increase interest rates to get inflation back down to its target rate of 2%. The year-over-year rate of inflation for the U.S. peaked at 9.1% in June 2022 before falling to 3% over the next year as the Fed continued to raise rates. For over a year now, the Fed has maintained its effective funds rate at 5.33%, up from a low of .05% during the COVID-19 pandemic.

[ii] At the same time, it reduced its asset portfolio by $1.78 trillion, or 19.9%.

[iii] The tighter monetary conditions have evidently had their desired effect. While inflation still has not returned to the 2% target, it has remained relatively stable between 3% and 3.5% over the last year.

While record inflation compelled the Fed to tighten monetary conditions starting in 2022, such actions can discourage investment and lead to a slower economy. This in turn can put their second mandate of full employment at risk. Economists visualize this inverse relationship between employment and inflation using the Phillips Curve. Notably, the Phillips Curve has not always held true. In the 1970s, for example, inflation and unemployment rose in tandem in what became known as “stagflation.” Figure 1 displays the Phillips Curve model for national and state-level unemployment and inflation data.

As unemployment peaked in April 2020 at 14.8%, year-over-year inflation reached a near all-time low and maintained levels under 2% during the recovery period. This held true at the national level and in Iowa. This trend can be largely attributed to the Federal Reserve’s expansionary policy tools, specifically cutting interest rates to near zero and expanding its asset purchase program of various securities by $4.8 trillion at its peak—over double its starting balance pre-pandemic. These actions stimulated economic activity for consumers and businesses but also led to high levels of consumer price inflation and asset inflation. As the Fed keeps interest rates high and reduces its balance sheet to stabilize inflation, the Phillips Curve predicts the labor market will react inversely.

To achieve a so-called “soft landing” whereby inflation returns to 2% without slowing down the economy too much and causing unemployment to rise, the Fed monitors both indicators carefully. Through most of its tightening regime, the Fed has managed to walk this tight rope, but in July, the nationwide unemployment rate rose to 4.3%—the highest it’s been since November 2021. Rising unemployment often directly precedes an economic slowdown or retraction.

[iv] Indeed, the recent rise in the United States unemployment rate triggered a major economic indicator of recession this month.

The labor market flashes warning signs.

The labor market has long been considered a crucial measure for the strength of an economy. A robust labor market can indicate increased output, consumer spending, business investments, and overall economic wellbeing. However, it is not always clear when the economy is in a recession. Economists consider a recessionary period has consisting of two consecutive declining negative quarters of gross domestic product. At least six months of data, sometimes even more, is required to even label an economic downturn as a recession. Monthly released unemployment data can provide reliable insight into the current state of the economy without waiting long.

The Sahm Rule, developed by formed Fed economist and senior economist at the

Council of Economic Advisers in the Obama administration, posits when the three-month moving average of the national unemployment rate is at least 0.5% higher over the last twelve months, the economy has entered recession. Since 1970, the United States has always entered or was already in a recession sometime after triggering the indicator’s 0.50 threshold; it reached 0.53 with the July BLS jobs report. However, indicators are never perfect, and this is the first time the U.S. has triggered this threshold since the pandemic. In fact, in an interview earlier this week, Claudia Sahm said, “This time, the economy does not look like it’s in a recession.” It will be crucial to revisit August’s data before establishing a definitive trend.

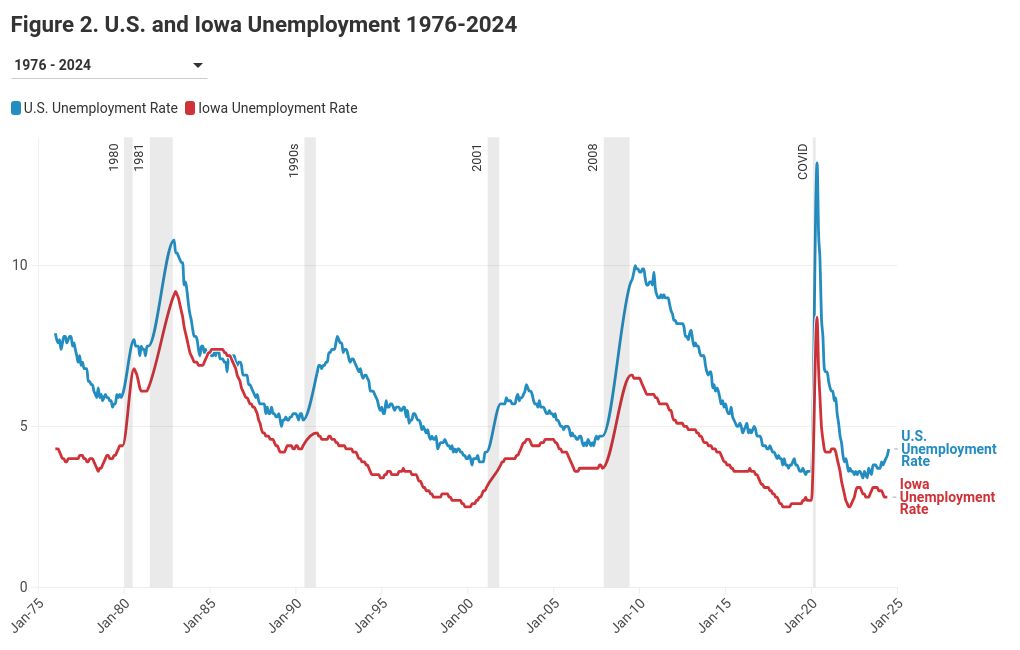

Economic models specifically utilize employment levels as an indicator of economic slowdown because weak labor markets typically signal a weak economy. Figure 2 illustrates historical and recent trends in unemployment, as well as the last six reported nationwide recessions in gray.

Historically, Iowa has trailed the United States in entering recessions; the national economy usually slows before Iowa’s economy does. The U.S. unemployment rate has risen sharply either shortly before or right at the start of each recession going back to 1980. Iowa’s unemployment rate has typically remained lower than the national rate but has generally followed the same trend. However, during this cycle a stark divergence has emerged between the United State and Iowa’s unemployment rates. As of July, unemployment has risen to 4.3% in the U.S. and 2.8% in Iowa. Based on this data alone, Iowa’s economy may remain strong even if the broader U.S. economy deteriorates. Though the Fed bases its policy decisions on the United State employment data, Iowans can monitor the economic conditions here at home using the BLS and LAUS employment data for the state of Iowa.

July Inflation Report: The U.S. vs. Iowa

In early 2021, inflation across the United States began to rise at rates far above the historic norm. In the Midwest, consumer prices have risen by 22.2% since March of 2020 when emergency fiscal and monetary measures went into effect to blunt the impact of economic shutdowns. As a result, the typical Iowa household must now spend $1,088 per month more than it did in 2020 to maintain the same standard of living. That same household has spent an additional $28,980 since 2020 to maintain the same standard of living. The cost increases have been led by a surge in housing, transportation, and food prices, which have risen by $375, $306, and $156 per month, respectively. While the rate of increase in prices has slowed, Iowans continue to spend more of their paychecks on necessities due to the inflation that has already hit. Figure 3 shows the cumulative increases in costs since 2020.

U.S. inflation cools while Midwest inflation rises.

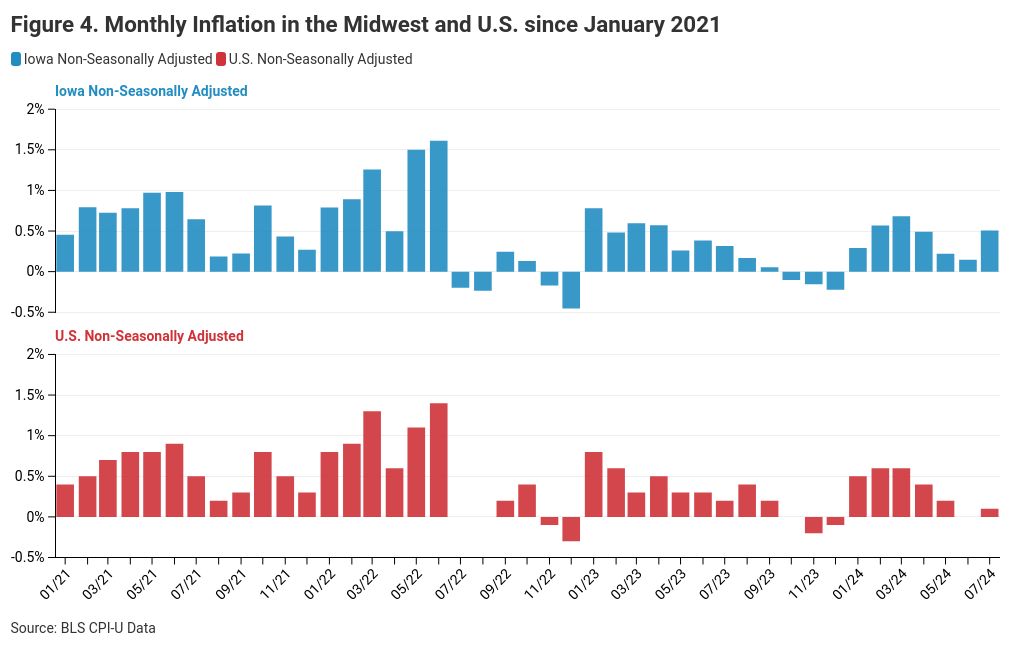

In July, month-over-month inflation fell in the U.S. but rose in the Midwest region. On a not seasonally adjusted basis, inflation 0.5% in the Midwest from June to July but rose just 0.1% in the U.S. The Fed looks to seasonally adjusted inflation data for the United States, a statistic not reported at the regional level. On a seasonally adjusted basis, U.S. month-over-month inflation came in at 0.2% in July, up from -0.1% in June. The annual inflation rate equals twelve months of month-over-month inflation summed. Therefore, following the trend in monthly inflation can help to indicate where annual inflation is headed in the future. Month-over-month inflation has come and gone in waves since the pandemic, as seen in figure 4.

Month-over-month inflation fell steadily from 0.8% in January 2023 to -0.2% by the end of the year. By June 2024, the cumulative effect of lower monthly inflation brought the annual inflation rate down to a low of 2.5% not seen in the Midwest since the previous June. National month-over-month inflation fell at a similar rate by the end of 2023, from 0.8% to -0.01%. In June, national not seasonally adjusted monthly inflation cooled at a quicker rate than the Midwest at close to 0.03%. In July, the Midwest, Midwest monthly inflation to 0.5% in July while the United States maintained a relatively low 0.1% increase.

While U.S. inflation continues to cool, Midwest inflation could be experiencing a return to higher rates. One month’s data does not establish a trend, but these numbers can reflect the broader impact of the Fed’s interest rate policy on the region. The Midwest has not been as fortunate as the broader United States, but there is still hope for a move back toward the Fed’s 2% inflation target, with future data being essential to determine a trend. The S&P 500 gained 1.7% in trading in response to the low inflation print.

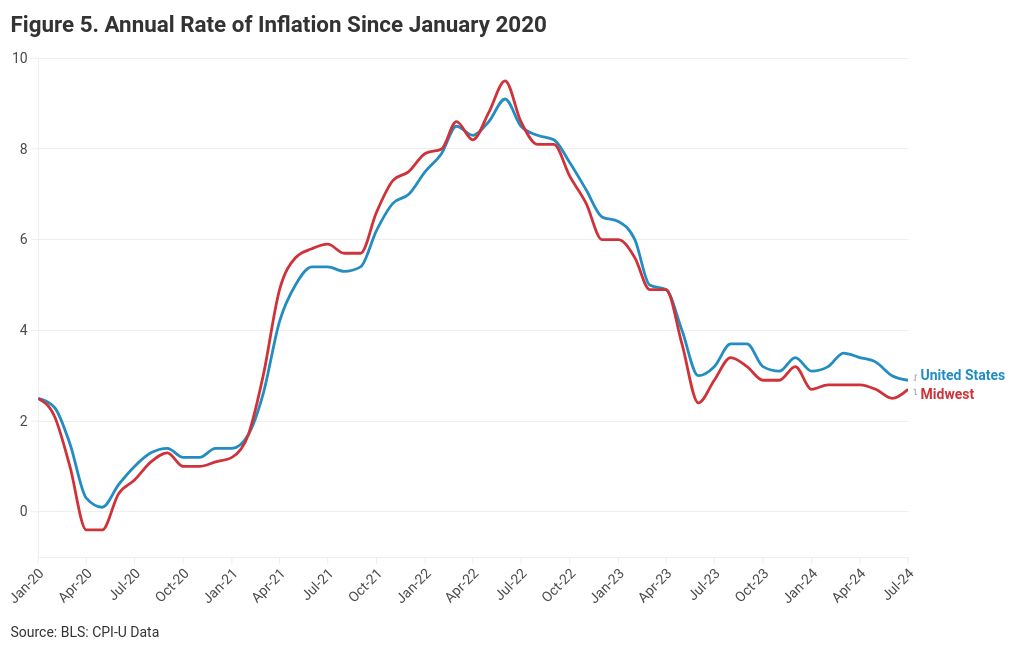

After rising by about 22% in the Midwest since the start of the pandemic, the cost of living will likely never return to 2020 levels. However, the rate of increase in prices has cooled. In the Midwest, annual inflation has remained mostly flat in 2024. It started at 2.7% in January, remained at 2.78% from February through April, down to 2.5% in June, with a recent uptick back to 2.7% in July. These year-over-year inflation figures reflect past changes. Since January 2024, the Midwest has consistently overperformed the U.S. regarding inflation with sizable differences ranging from 0.4% to 0.7%. The most recent print has narrowed this gap between Midwest and U.S. month-over-month inflation to 0.2%, suggesting that while nationwide inflation falls, the Midwest is stabilizing at 2.7%.

Housing, services, fuel, & utilities drive inflation.

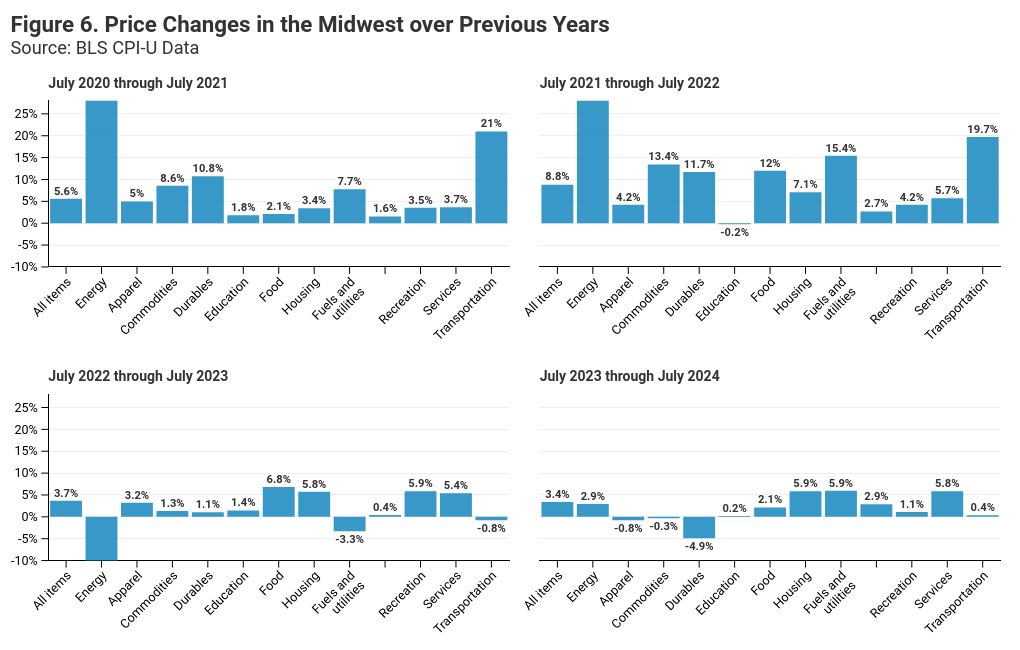

The cost of housing, services, fuel, and utilities has led the increase in prices in the Midwest in 2024. From July 2023 to July 2024, the cost of housing rose 5.88%, services by 5.84%, and fuel and utilities by 5.94%. Common Sense Institute reported a similar price increase for housing and services in its past report,

Inflation in the Midwest: May 2024, signaling that these industries are not cooling as quickly as the rest of the economy. Sticky inflation in the services sector could be a result, at least in part, of the tight labor market in Iowa and the Midwest. A tight labor market pushes up wages, which in turn pushes up prices. This is especially pronounced in the services sector where labor costs comprise a large portion of operating expenses.

As the Federal Reserve continues to tackle inflation at a nationwide level, its efforts are being thwarted by these essential costs unwilling to comply. Meanwhile, the cost of durables fell 4.88%. Notably, food prices are continuing to rise at a slow but consistent pace, increasing 2.2% over the past year in the Midwest compared with 6.8% a year ago and 12% the year before that. The cost of commodities again fell in June and July in the Midwest. This is good news for consumers but may weigh negatively on Iowa’s commodities heavy economy. Figure 6 shows the year-over-year inflation rate in the Midwest by various consumer categories.

The Federal Reserve hasn’t achieved its 2% inflation rate mandate, but it made significant progress in that direction. The United States has been able to cool inflation to levels not seen since early 2021. This indicates the Fed’s monetary tightening is having its desired effect. However, recent upticks—particularly in the Midwest—can indicate that cooling has hit a resistance point. Both the U.S. and the Midwest would need to experience consistent deflation to reach the Fed’s 2% target by the end of the year. However, keeping monetary conditions tight if unemployment rises could strain the economy and stall economic recovery. Thus, the Fed may be willing to cut rates without a return to 2% inflation if unemployment rises. Such action could trigger another bout of inflation, resulting in both high unemployment and high inflation like the United States experienced in the 1970s. To achieve its desired “soft landing,” the Fed needs to get inflation under control without a sharp rise in unemployment. In this regard, the U.S. inflation data brings optimism, but Iowa’s inflation is headed back in the wrong direction. Nonetheless, Iowa has maintained an inflation rate consistently lower than the U.S. rate, as seen in figure 5.

July Jobs Report: The U.S. vs. Iowa

In July, U.S. employment levels grew by 114,000 jobs. At the same time, unemployment increased by 0.2% from 4.1% to 4.3%. According to the BLS establishment survey, Iowa employment fell by 1,500, or –0.09%, wiping all gains since February 2024. It’s unemployment rate remained at 2.8%.

The household survey data has trended in a similar direction, with employment falling by 3,565, or –0.21%. The July household survey employment numbers, 1,638,041, are the lowest since November 2021. At the same time, Iowa’s labor force also fell by 2,592 to a level not seen since May 2021. Simultaneous job and labor force losses did not impact the state’s unemployment rate—keeping it at 2.8%. It ranks 7

th compared to other states, unchanged from the prior month. Maintaining a relatively low unemployment rate is a good indicator of the strength of Iowa’s jobs market, but the downward trend in employment and labor force is troubling. If the decline in both labor force and employment persists, it could signal deeper structural challenges in Iowa’s labor market.

This divergence in the data has also become increasingly apparent following Iowa’s pandemic recovery. One reason for this divergence is how both surveys track employment. The establishment survey gathers data directly from employers, while the household survey utilizes Current Population Survey (CPS) data from households. This leaves a gap in reporting specifically regarding multiple jobholders.

According to the July National CPS release, 8,473,000 individuals were working multiple jobs.

[v] This is 311,000, or 3.81%, more than July 2023. In terms of percent total employed, workers with multiple jobs made up 5.3%, up 0.2% since last year.

[vi] It is worth nothing that the United States reached a peak number of 8,565,000 individuals working multiple jobs in December 2023; this is the highest level since the data was first collected in 1994. The last available data for specifically Iowa was in 2022 and recorded 7.6% of the labor force as having multiple jobs.

[vii] Recent spikes in multiple jobholders can be attributed to rising costs, which force many families to sacrifice their time for extra income. August’s CPI data can shed light into how inflation is trending, and how this situation may fare in the months to come.

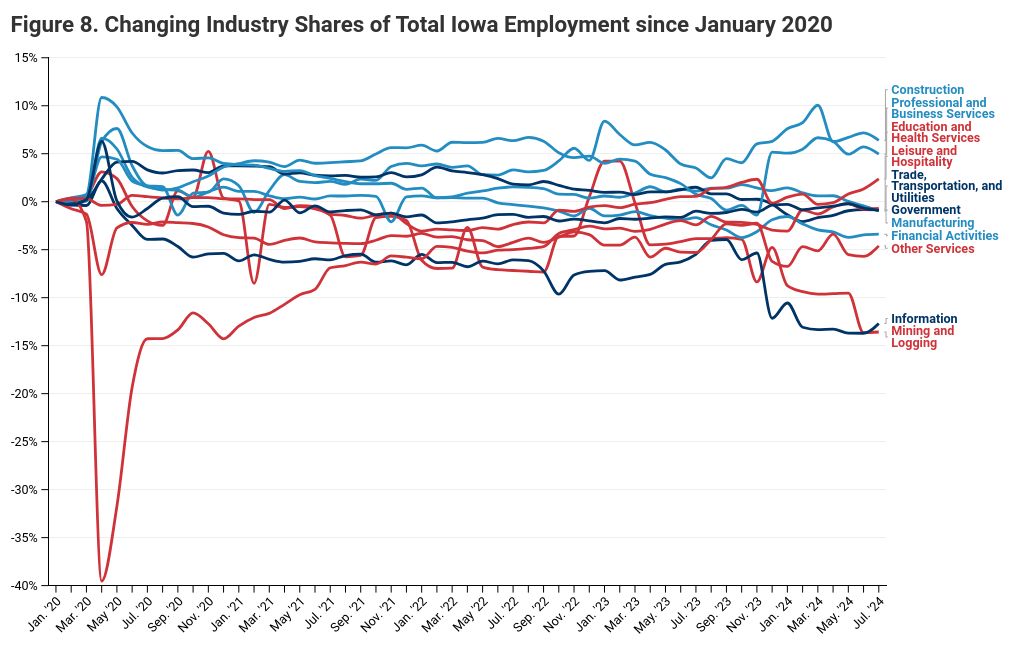

A Deeper Dive into Iowa Industries

- Based on the establishment survey, the net decline of 1,500 jobs in July was driven by net job losses in 5 of 11 major sectors.

- Manufacturing lost 1,400 jobs for a 0.61% decline.

- Professional and Business Services lost 1,200 jobs for a 0.80% decline.

- Construction lost 700 jobs for a 0.81% decline.

- Government lost 800 jobs for a 0.30% decline.

- 3 major sectors saw a net increase in jobs from June to July.

- Education and Health Services gained 2,300 jobs for a 0.95% increase.

- Other Services gained 600 jobs for a 1.07% increase.

- Information gained 200 jobs for a 1.10% increase.

- “Mining and logging,” “Financial Activities,” and “Leisure and Hospitality,” did not experience any changes in employment.

Iowa has performed historically well in maintaining a labor force participation rate (LFPR) above the U.S. average, but it has recently trended downwards. In August, the LFPR grew by 0.01% across the U.S. but fell by 0.01% to 66.4% in Iowa, down from 66.5% in June. Iowa’s LFPR has steadily declined from 68% in May 2023, revealing a clear downward trend as new data emerges. At the same time, employment dropped, signaling that workers are both losing jobs and exiting the workforce entirely. This can be a result of many factors, such as Iowa’s ageing population, out-migration, and slowdowns in important industries that fuel employment in Iowa, such as construction and professional business services—Iowa’s two largest sectors by employment. Broader implications of relatively high rates of multiple jobholders can also inflate the LFPR, given that the household survey does not differentiate between single and multiple jobholders.

Based on the July employment print, the Fed’s rate hikes may be starting to impact the labor market. On the national level, unemployment rose to 4.3% but was met with increasing labor force numbers. Iowa was able to keep consistent unemployment numbers at 2.8% but experienced even lower labor force participation rates, dropping another 0.1% and continuing its downtrend since May 2023. Despite the positive unemployment print, Iowans are leaving both jobs and the labor force. If this trend continues, it could signify the looming impacts of the Fed’s headstrong battle against record inflation and a possible slowdown in the state’s economy.

Conclusion

The July inflation and employment data reveal mostly concerning economic trends for Iowa and the United States. While the Fed’s policy of maintaining high interest rates has successfully reduced inflation below 3% for the first time since 2021, the rising trend in national unemployment is counterintuitive to growth. This suggests that as inflation cools at the national level, the labor market is beginning to weaken—similar to what is expected on a Phillip’s Curve. This is especially evident in the United States, where unemployment has reached 4.3%, suggesting an uptrend in the data. Given that Iowa has historically followed, not led, the broader United States into a recession, data from the state also prove concerning. In July, Midwest inflation increased 0.2% to 2.7% with employment numbers in Iowa falling. Consistently falling labor force participation numbers also signal that the Iowa economy is losing employees in the labor force at a troubling rate—a trend not seen at the national level. Coupled with recession indicators like the Sahm Rule, the United States has not produced enough evidence to expect a soft landing. If new national data in the coming months continues to lead unemployment levels higher, then Iowa should brace for similar results. Regardless of the Fed’s next steps, its current efforts to cool inflation since 2021 through rate hikes appear to be starting to impact the labor market. This rightly raises concerns over an economic slowdown. Iowans should continue to watch national and regional inflation and employment data each month for clues about the direction of the economy and future Fed action.

END NOTES

[i] Cook, Lisa D. “The Dual Mandate and the Balance of Risks.” Board of Governors of the Federal Reserve System, March 25, 2024. https://www.federalreserve.gov/newsevents/speech/cook20240325a.htm#:~:text=The%20Fed's%20modern%20statutory%20mandate,to%20as%20the%20dual%20mandate.

[ii] Board of Governors of the Federal Reserve System (US), “Federal Funds Effective Rate [FEDFUNDS],” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/FEDFUNDS.

[iii] Board of Governors of the Federal Reserve System (US), “Assets: Total Assets: Total Assets (Less Eliminations from Consolidation): Wednesday Level [WALCL],” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/WALCL.

[iv] Richmond Federal Reserve. “Unemployment Changes as Recession Indicators.” Economic Brief, no. 23-13, April 2023. https://www.richmondfed.org/publications/research/economic_brief/2023/eb_23-13.

[v] Board of Governors of the Federal Reserve System (US), “Multiple Jobholders,” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/LNS12026619.

[vi] Board of Governors of the Federal Reserve System (US), “Multiple Jobholders as a Percent of Employed,” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/LNS12026620.

[vii] U.S. Census Bureau. “Current Population Survey: Displaced Worker, Employee Tenure, and Occupational Mobility Supplement Microdata.” data.census.gov, 2022. https://data.census.gov/mdat/#/search?ds=CPSDISWORKJOBTEN202201&cv=PRSJMJ&rv=ucgid&wt=PWCMPWGT&g=0400000US19.