Iowa’s policymakers, providers, and insurers operate within a state comprised of an aging population and large rural areas. According to the Iowa Department of Justice, the state ranks 16

th nationally for the number of residents 50-years-old and over.

[ii] Approximately 18% of Iowa’s more-than-three-million residents are 65 years old and older while 23% are under 18 years old. The average life expectancy in Iowa is 78.12—21

st highest in the country. In addition, the United States Department of Agriculture (USDA) considers 77 of the state’s 99 counties “rural” based on the amount of open countryside and rural towns.

[iii] An astounding 22 of these rural counties have 100% of the population residing in a rural area.

[iv] Other factors also help set the stage for the Iowa healthcare industry. Its diabetes prevalence of 8.5% puts the state at 28

th highest in the country, and approximately 37% of the state’s population is obese, giving it the 13

th highest obesity rate in the country, to name just two.

[v] While not directly caused by the healthcare system per se, these and other factors significantly influence Iowa’s particular healthcare needs and frame the backdrop for this report.

Iowa needs a healthy population to thrive. To achieve that, Iowans must have access to quality healthcare. The ability of the state’s healthcare system to deliver that in the context of its unique demographics and characteristics depends on several factors. Access to quality care starts with the existence of providers and a workforce to support them. For patients to access providers’ services, they must possess means to pay. This depends largely on healthcare costs and the insurance market. And in the case of Iowa, to ensure access across the state the healthcare system must supply rural areas with sufficient healthcare resources.

This report thus explores and presents data on Iowa’s healthcare business climate, healthcare expenditures, insurance, and rural healthcare. In doing so, it highlights Iowa’s unique healthcare landscape to help public- and private-sector decision makers understand the state’s challenges and identify where to focus solutions to improve the state’s healthcare system.

Key Findings

- Thanks primarily to rising operating costs, over a third of Iowa hospitals and 60% of rural hospitals operated at a loss in 2022.

- Over the last 15 years, 250 more healthcare facilities in Iowa have closed than have opened, with mental health centers leading all provider types in net closings.

- Vacancies for hospital personnel in Iowa increased by 73% between 2020 and 2021.

- With a 270% increase, Iowan’s healthcare costs rose at about triple the rate of inflation in the three decades from 1991 to 2020.

- With an increase of 456%, home healthcare saw the largest increase in healthcare spending in Iowa between 1991 and 2020.

- Despite an overall increase in healthcare spending, at $9,200 per person, Iowans spend about 5% less on healthcare than the average American.

- Between 2013 and 2022 after the passage of the Affordable Care Act, the rate of uninsured Iowans dropped from 8.1% to 4.5%, making Iowa 7th lowest in the nation.

- The privately insured bear a large share of the burden from rising healthcare costs, with private insurers now paying 263% more for hospital services than Medicare.

- From 2009 to 2022, the total cost of health insurance in Iowa increased 67%, and deductibles rose 106%.

- As of 2022, Iowans have the fourth largest percent employee contribution (25%) to employer sponsored health insurance of any state.

- Rural Iowa has 17% fewer physicians per capita than its urban areas.

- In Iowa, 62 of the 77 rural counties (and 9 of the urban counties) do not have a practicing OBGYN.

- Since 2015, the rate of premature deaths per 100,000 Iowa residents has risen by 9% in urban areas and by 18% in rural parts of the state. Drug overdose deaths from fentanyl are a major contributor to the increase.

- While Iowa’s healthcare system faces tremendous challenges, it still ranks 2nd most competitive in CSI’s Healthcare Competitiveness Index when compared with the other 49 states and D.C.

- The Iowa state legislature has promulgated 21 legislative reforms since 2018 to address the challenges to the state’s healthcare system.

CSI Healthcare Competitiveness Index

Before delving into the minutia of Iowa’s healthcare system, Common Sense Institute’s Healthcare Competitiveness Index provides perspective on the state of healthcare in Iowa relative to other states. Each year, CSI issues a Free Enterprise Report, which assesses each state’s competitiveness relative to 49 other states and the District of Columbia on eight policy areas: education, energy, housing, infrastructure, public safety, government budget, taxes, and healthcare. First, the index scores each state’s relative competitiveness based on several metrics under each of the eight categories. Then, the index ranks states under each of the eight categories and equally weights the results from each category to assign the overall Free Enterprise Index ranks. The CSI State Healthcare Competitiveness Index consists of four metrics:

- Percent of residents privately insured

- Percent of residents with employer-provided insurance

- Spending per capita on Medicare & Medicaid

- Number of active physicians per 100,000 residents

While Iowa faces many of the same challenges as the rest of the nation in providing quality, affordable healthcare to all its residents, it has maintained a competitive healthcare landscape relative to other states based on these four metrics. The state currently ranks second nationally on the overall healthcare competitive index and has ranked either first or second every year since 2012, as shown in figure 1.

[vi]

While useful for providing a general sense of a state’s performance across multiple broad categories, indices like CSI’s Free Enterprise Report index lack the detailed insight of a more in-depth study. Iowa may rank well based on the four metrics that comprise CSI’s Healthcare Competitiveness Index, but it may perform poorly by other metrics not reflected in the index. Even if an index includes more metrics, it does not typically contain a detailed survey of the underlying data for each metric.

In addition, such indices measure

relative performance but fail to convey

absolute performance. A state may perform poorly by objective measures but rank well on a relative basis if all states in the index perform more poorly. For example, CSI’s Healthcare Competitiveness Index rewards states for having more physicians per 100,000 residents than other states. That means a state’s index rank could improve while its number of physicians per 100,000 residents declines if other states lose physicians more rapidly. Even while in decline, a state may remain competitive on a relative basis within a generally declining national healthcare system.

This report aims to achieve what an index does not. In addition to comparing Iowa with other states, it also explores Iowa’s healthcare performance on an objective or absolute rather than relative basis. Through hard data, the report illuminates strengths and weaknesses across the state’s healthcare economy. It then surveys that data fully and transparently, illustrating how Iowa’s performance today compares with its past performance.

Iowa’s Healthcare Business Climate & Outlook

The healthcare business climate in Iowa is under significant economic pressures, marked by both opportunities and challenges. Recent years have seen a troubling trend of increasing operational costs and facility closures. This has put the state’s hospitals under significant financial strain, undermining a critical pillar of the healthcare system. A workforce shortage in the face of increasing demand for services compounds these difficulties. Nonetheless, Iowa’s healthcare industry remains a major driver of jobs and economic output in the state. This section delves into the current state of Iowa's healthcare business climate, examining the factors influencing hospital operations, the trends in facility closures, and the outlook for the healthcare workforce in the state.

Iowa’s healthcare industry employs 210,700 people—10% of Iowa’s total workforce.

[vii] More than 30% (69,100) of these healthcare workers are employed in ambulatory health care services, which includes clinics, such as physicians and dentists, medical laboratories, and home health care services. Adding 10 jobs in the healthcare industry creates an estimated 9.4 more jobs across Iowa’s economy.

[viii] In addition, the healthcare sector generates $14.3 billion dollars a year in GDP, representing 6% of total GDP in the state. Iowa ranks 8

th lowest in the nation for healthcare GDP as a share of total economic output. As indicated by the estimated multiplier effect, for every one dollar of GDP produced by the healthcare industry, Iowa’s GDP increases by an additional $0.21.

[ix]

| Table 1. Iowa Healthcare Employment & GDP Contribution, 2022 |

| Type |

Employment (thousands) |

GDP Contribution (millions) |

| Ambulatory Health Care Services |

69.1 |

6514.9 |

| Hospitals |

39.7 |

3873 |

| Nursing and Residential Care Facilities |

50.6 |

2518.1 |

| Social Assistance |

51.3 |

1444.1 |

| Total Health Sector |

210.7 |

14,350.10 |

| Total Iowa |

2,114.00 |

238,342.30 |

| Healthcare Share of Total |

9.97% |

6.02% |

| Multiplier |

1.94 |

1.21 |

| Source: BLS and REMI. |

|

|

The state has 118 hospitals, 2,305 primary care physicians, 4,185 registered nurses, 2,268 dentists, and 6,358 mental health care providers as well as many other contributing members of the healthcare system.

[x] While there are 95 health insurance companies licensed in Iowa, only three of them participate in the Individual Health Insurance Marketplace, and a small number of these companies cover most of the market.

[xi] Wellmark Blue Cross and Blue Shield, the largest insurer, has a market share of 80%, followed by UnitedHealth at 11% and HealthPartners at 3%.

[xii]

Iowa hospitals face increasing financial vulnerability.

Iowa’s network of hospitals plays a central role in providing for the healthcare needs of the state’s population, and their continued operation depends largely on their financial health. Nationally, more and more hospitals have seen annual expenses exceed annual revenues, as over half of all hospitals in the U.S. reported operating at a loss in 2022.

[xiii] Though better, the situation proves similarly bleak in Iowa, particularly for rural parts of the state. In 2022, 45% of Iowa hospitals operated at a loss when measured using operating revenues, and 36% operated at a total loss including all revenue sources. An increase in operating expenses rather than a decrease in revenue has driven the increased rate of operating losses.

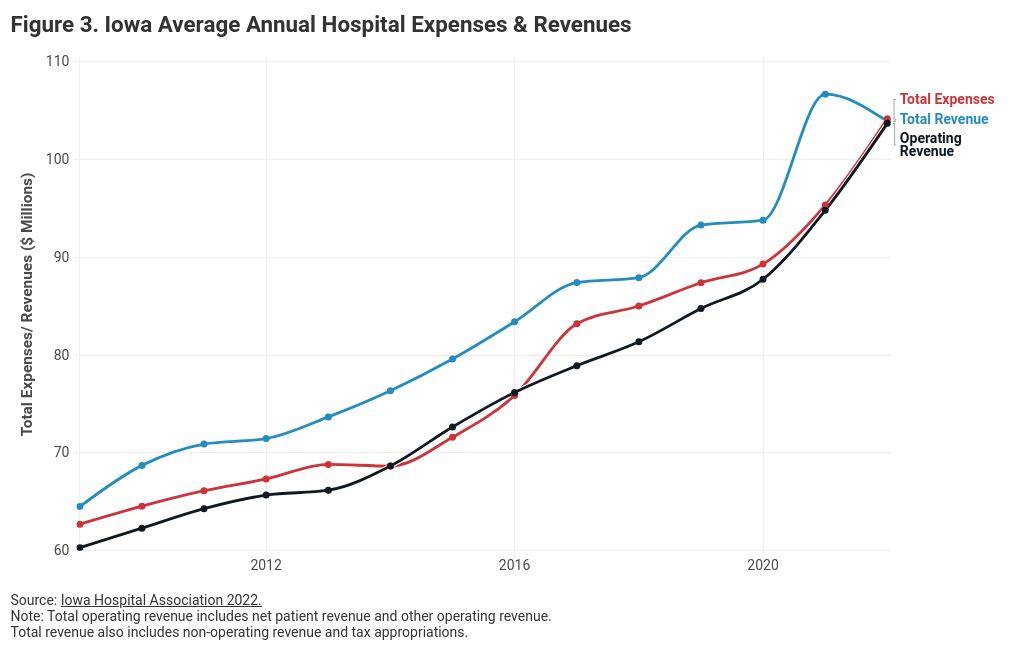

Between 2009 and 2022, average annual hospital expenses in Iowa increased by 66% from $63 million to $104 million as shown in figure 3.

[xiv] Between 2019 and 2021 alone, labor costs, which comprise more than half of hospitals’ total expenses, increased by 19%.

[xv] As of 2022, average total expenses have now surpassed both average total operating revenue and average total revenue for hospitals in Iowa. Operating revenues include patient revenue and other operating revenue, while total revenue includes all operating revenue as well as grants, tax revenues, and profits from other activities that can offset losses on patient services. Since these additional sources of revenue are not guaranteed, it is important to consider the relationship between operating revenues and expenses when evaluating Iowa hospitals.

At first glance, figure 3 appears to show a drop in total revenue as the driver of increased operating losses. In fact, the growth in operating expenses between 2020 and 2022 well outpaced the growth in total revenue. Over the two-year period, total expenses grew by 16.64% while total revenue grew by only 10.77%. The percentage of hospitals in Iowa operating at a total loss dropped significantly in 2021 due to non-operating Covid-related revenue, primarily through the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which appropriated more than $170 billion in relief funds to hospitals.

[xvi] The effects of this 2021 federal aid can be seen in figures 2 and 3. As that one-time aid ran out in 2022, revenues dropped off but remained near their trendline. In contrast, expenses surged above their historic trend in 2021 and 2022.

To accurately compare the margins of hospitals of varying sizes, figure 4 illustrates average hospital operating profits (operating revenues minus total expenses) as a percent of average hospital revenues aggregated by county. In 2019, the average hospital profit as a percent of revenue by county ranged from -31% to 12% across the state with an average of 1.6%.

[xvii] These margins are unsustainable for many hospitals and should be considered when passing policies that have the potential to impact hospital revenues or expenses.

Provider expenses have increased substantially since 2009, with the most significant rise occurring since the pandemic. While rising labor and material costs contribute to this trend, an increased administrative burden on providers is also a substantial factor. Historically, healthcare administrative costs in the U.S. were estimated around 10%, however a recent CAQH report estimates that administrative costs have surged to nearly 22% of total healthcare expenditures since the pandemic.

[xviii] This increase is primarily due to the complexity of the healthcare and insurance systems. Administrative complexity, along with other forms of inefficiency such as overtreatment, care coordination failures, and execution failures, are all considered wasteful as they do not provide health benefits to individuals despite incurring costs. Further research could examine and quantify the cost burden of these wasteful requirements, including administrative burdens, and their impact on Iowa’s healthcare system specifically. Regardless of the reason for hospitals’ financial woes, no non-profit or for-profit entity can continue to operate at a loss indefinitely without closing.

More Iowa healthcare facilities are closing than opening.

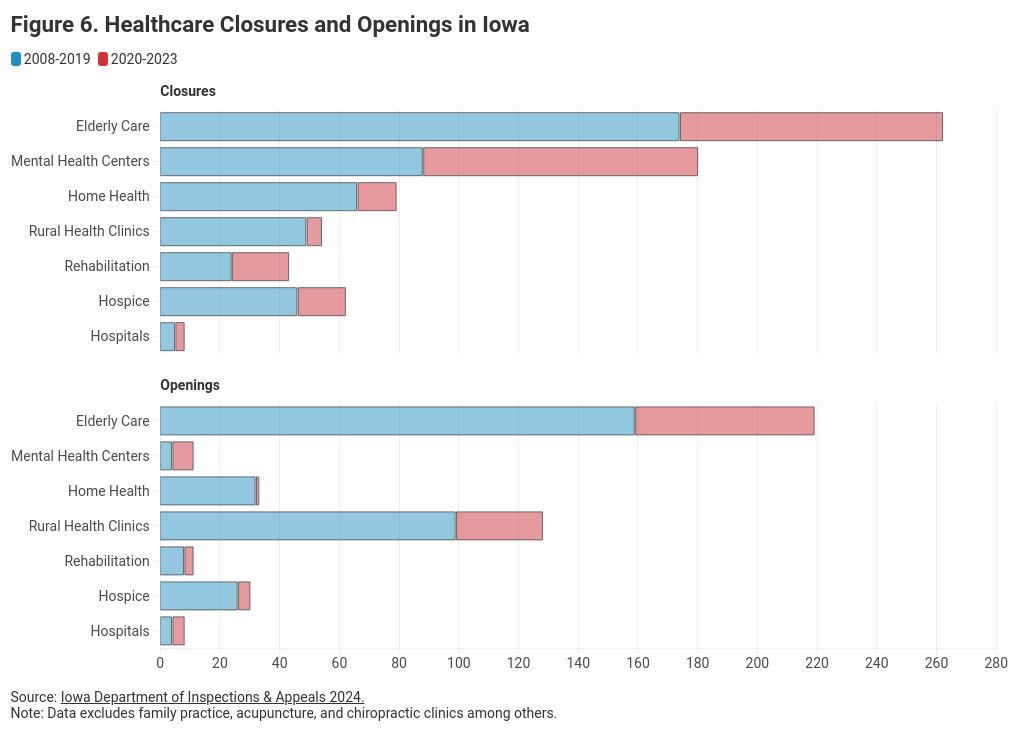

As more Iowa hospitals experience operational losses, hospital closures have continued across the state, a fate they share with other major types of healthcare facilities. According to facility data from the Iowa Department of Inspections and Appeals (IDIA), there have been more than 600 healthcare facility closures since 2008 — excluding family practice, acupuncture, and chiropractic clinics — and fewer than 450 openings.

[xix] Figure 5 illustrates the trend in healthcare closures and openings between 2008 and 2023.

While all types of healthcare facilities have seen both openings and closures over the last 15 years, closures have outpaced openings in all but three years: 2016, 2019, and 2020. In 2016 the state had the same number of openings and closures. An anomalous increase in closures occurred in 2021 and 2022 while openings also decreased. While the data appears to have moved toward normalization in 2023, these two years contributed significantly to the total net closures over the period. Breaking down the data by type of facility provides more insight into the specific source of closures. Figure 6 shows the number of closures and openings by category.

Of the seven healthcare facility types shown in figure 6, five have seen a net decrease since 2008: elderly care, home health, hospice, mental health centers, and rehabilitation centers. Rural health clinics have experienced more openings than closures and there have been the same number of hospital closures as openings.

Elderly care—which includes nursing homes, assisted living, and residential care facilities—saw the most openings and the most closures of any category.

[xx] Two hundred and sixty-two elderly care facilities closed over the 15-year time span with 88 of those occurring in just the last three years. Iowa is not alone in the heightened rate of elderly care closures. Nationwide, 550 skilled nursing facilities (one type of elderly care) closed their doors between 2015 and 2019, and an additional 579 closed between 2020 and 2022.

[xxi] However, 159 elderly care facilities opened in Iowa between 2008 and 2019 and 60 opened between 2020 and 2023.

[xxii] Although many new elderly care facilities have opened, the specific distribution of location and types of facilities closing and opening remains unclear.

Mental health centers experienced the second highest number of closures and by far the highest number of net closures. These facilities include community mental health centers, residential and intermediate care facilities for the intellectually disabled, and psychiatric medical institutions for children.

[xxiii] Of the 180 closures of this type that occurred between 2008 and 2023, 92 of them came in the last three years. Unlike the elderly care facilities, only 11 mental health facilities opened between 2008 and 2023, creating a net decrease of 169 facilities. That equates to a stunning 94% overall decrease. Additional research is needed to understand the cause of this large number of net closures, as it was not readily apparent in the data.

The remaining categories saw 79 home health closures and 33 openings between 2008 and 2023, 54 rural health clinic closures but 128 openings, 43 rehabilitation clinic closures with 11 openings, 62 hospice closures with 30 openings, and 8 hospital closures.

[xxiv] While 8 new hospitals also opened during this time, the total number of hospital beds in Iowa decreased from 9,740 in 2015 to 8,698 in 2022—a 10% reduction.

[xxv] The Center for Healthcare Quality & Payment Reform estimates 28 Iowa hospitals have financial reserves inadequate to cover their losses for more than 6-7 years.

[xxvi] Ten of them lack the financial reserves necessary to cover their losses for more than 2-3 years. These data signal a loss of access to hospital care in the state.

Iowa’s healthcare industry has an aging workforce.

In addition to sufficient revenues, providers need a workforce capable of meeting patient demand for services. Unfortunately, current workforce trends indicate a significant shortage will emerge in upcoming years as the supply of workers continues to decrease amidst an increase in demand for these positions. According to data released by the US Department of Health and Human Services, the number of vacancies for hospital personnel in Iowa increased from 4,091 in 2020 to 7,079 in 2021, a 73% increase.

[xxvii] Of the 2,942 additional vacancies, 1,363 were for nursing positions (RN, LN, and Nursing Assistive Personnel), and 1,307 were for positions other than physicians, nurses, technicians, and pharmacists. These hospital vacancy data illustrate the need for nurses, administrative personnel, and lower wage health workers in the state.

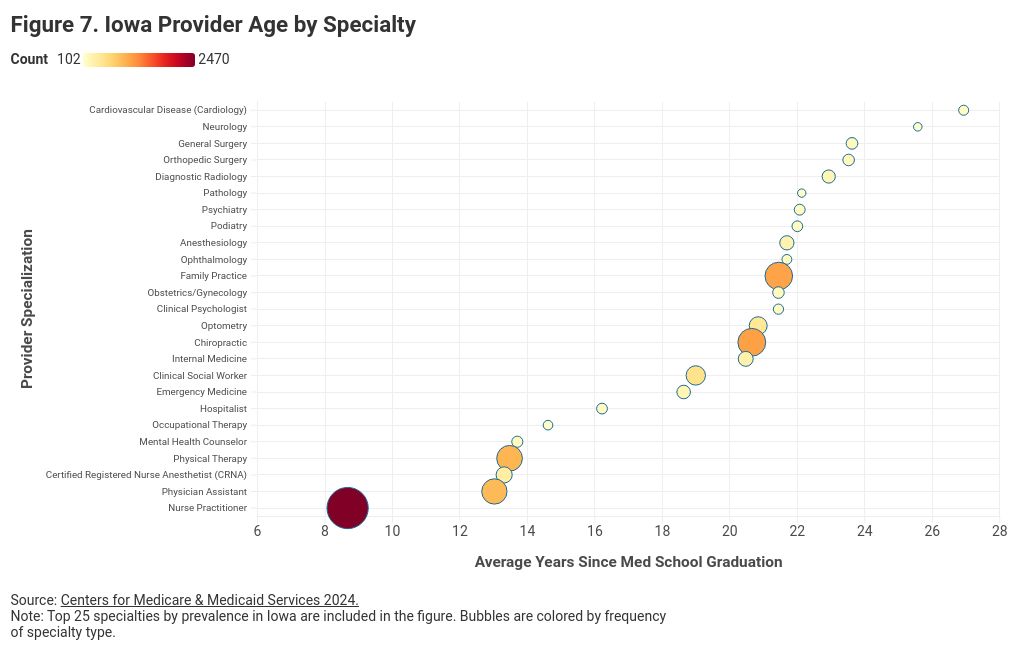

The age of providers can serve as a leading indicator of future workforce supply and help predict where a shortage of healthcare professionals might appear in the future if new workers do not replace aging workers. Using the number of years since graduation from med school as a proxy for age, figure 7 illustrates the variation in average age by provider type in Iowa.

[xxviii]

With a wide range of average provider age, the data show signs of encouragement and areas for concerns. Nurse practitioners, for example, are an average of 12 years younger than family practice providers. This indicates that providers are moving away from family practice and towards nurse practitioners. The 2,470 nurse practitioners in Iowa graduated less than nine years ago on average. This is both the largest cohort of healthcare workers and the youngest, suggesting strong supply for years to come. Conversely, Iowa’s cardiologists, neurologists, general surgeons, orthopedic surgeons, and diagnostic radiologists are aging out of the workforce rapidly. To continue meeting Iowans’ healthcare demand, the industry will need to replace these ageing providers as they retire, otherwise these areas could also see increased shortages.

While not listed in figure 7, lower wage healthcare positions such as medical assistants, home health aides, and nursing assistants serve critical roles in the healthcare industry. A report by Mercer projects Iowa will have a shortage of 36,000 low-wage health workers by 2026.

[xxix] In other words, the projected supply of low-wage healthcare workers is significantly below the projected demand for these positions. While the report also expects many states to have significant gaps in registered nurses and mental health providers—in some cases upwards of 10,000 nurses and 9,000 mental health providers—it expects Iowa to have a shortage of only 1,000 registered nurses and a surplus of 630 mental health providers by 2026.

Though Iowa’s healthcare workforce has strengths, policymakers and the industry should continue to seek ways to fill the healthcare workforce pipeline so younger workers can help meet current demand and fill the gap left by retiring professionals. The section of this report entitled “Recent Public Policy Changes” goes into more detail on state laws and regulations adopted by Iowa’s policymakers in recent years to help address healthcare workforce needs. Additional research could help determine the extent to which workforce shortages have contributed to closures, if at all, and which additional policy changes could further dampen future workforce shortages.

Healthcare Expenditures & Insurance

The presence of adequate healthcare providers alone does not ensure access for all Iowans. To access providers’ services, patients must have the means to pay for those services. While under certain circumstances patients can receive healthcare services without insurance and even without payment, the healthcare system cannot continue to operate without sufficient revenue. Indeed, as in any market, prices signal to healthcare providers which services and how much of each service to offer. Depending on the provider and the services rendered, revenue may come from a third party like an insurance company or Medicare, from grants or donations, or directly from the patient in the form of payment for services. In America’s healthcare market today, heavy government interventions distort market forces, leading to high prices, shortages, and other challenges. However, this report does not evaluate the merits or faults of specific interventions. Instead, it explores data on healthcare expenditures and insurance coverage to help identify where distortions and other imbalances might exist in Iowa’s healthcare marketplace. This section describes the composition and trends of healthcare expenditures in Iowa, how those expenditures are financed, and how the cost of health insurance has evolved.

Iowans' healthcare spending is up, but lower than others.

Health expenditures represent the amount of money spent on all health-related activities and includes spending from all sources such as personal, insurance, and government. Iowans spent $29 billion on healthcare in 2019, or an average of $9,193 per person. This is slightly lower than the national average of $9,671 per person as seen in Table 2.

| Table 2. Total Healthcare Spending by Category (2019, Millions) |

| Item |

Iowa |

US |

| Dental Services |

$417 |

$436 |

| Durable Medical Products |

$158 |

$174 |

| Home Health Care |

$183 |

$344 |

| Hospital Care |

$3,848 |

$3,636 |

| Nursing Home Care |

$780 |

$531 |

| Residential, and Personal Care |

$496 |

$596 |

| Other Professional Services |

$363 |

$339 |

| Physician & Clinical Services |

$1,945 |

$2,339 |

| Prescription Drugs and Other Non-durable Medical Products |

$1,002 |

$1,277 |

| Total Personal Health Care Spending |

$9,193 |

$9,671 |

| Source: Iowa Hospital Association, "Health Expenditures by State of Residence." |

|

|

| Note: Hospital categories include Critical Access Hospitals (CAH), Rural Hospitals, Rural-Referral/Urban Hospitals (RRU), and VA and Other Hospitals. The Other hospitals include rehabilitation and select specialty hospitals. |

Broken out by type of care, Iowans spend more on hospital care, nursing home care (6

th highest of any state), and other professional services than those in the rest of the country. They spend less on dental services, home health care, physician and clinical services (7

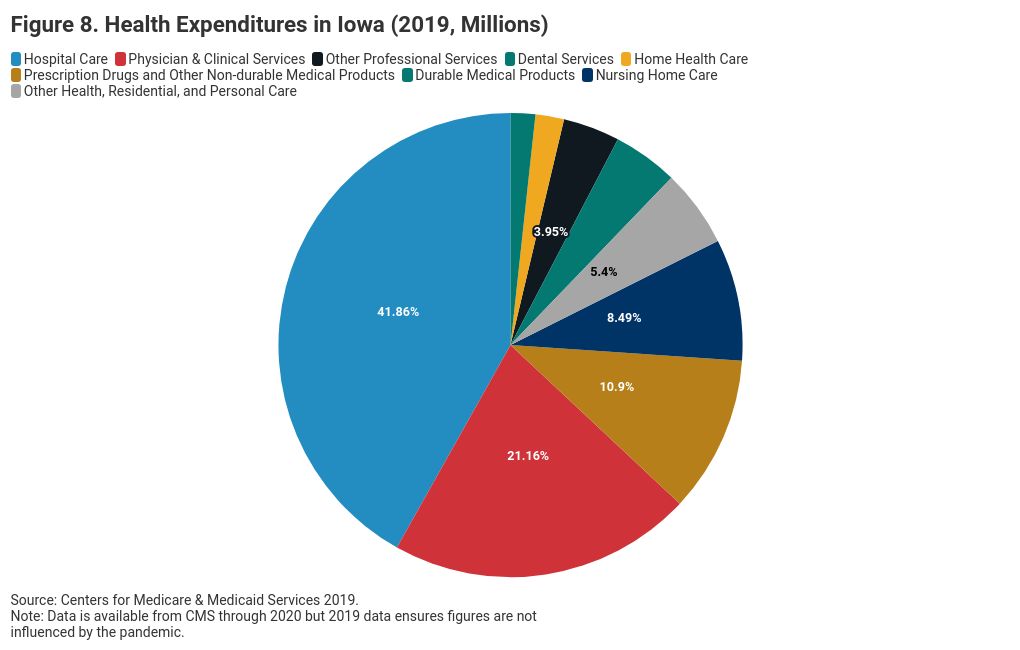

th lowest of any state), and pharmaceuticals. At 42% of total healthcare spending, hospital care is the largest category of healthcare spending for Iowans followed by physician & clinical services at 21%, and pharmaceuticals at 11%. See figure 8.

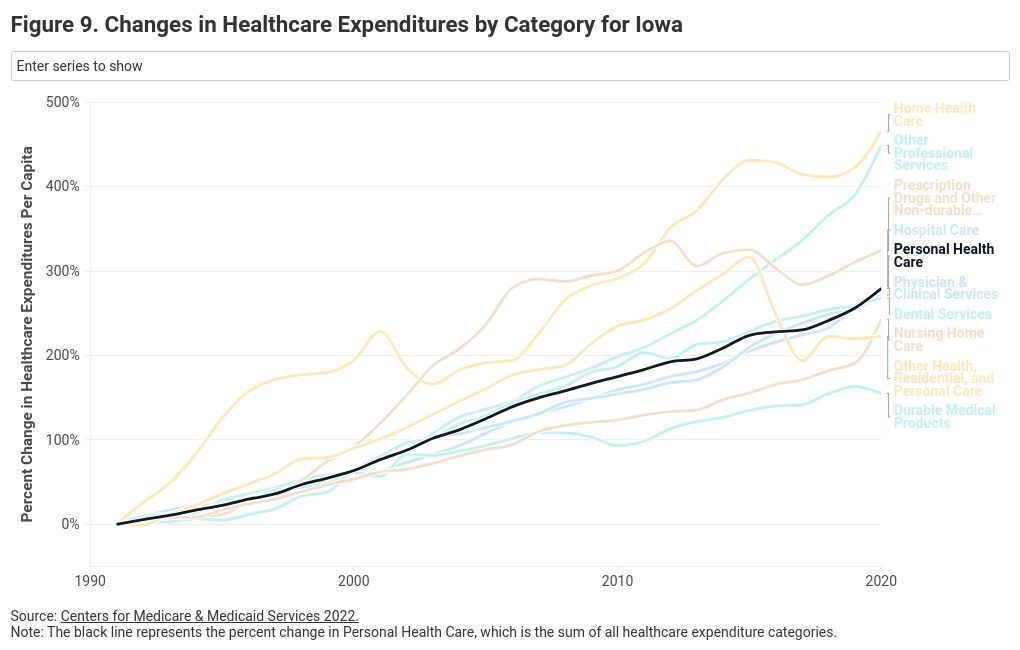

Spending on all categories of health goods and services has increased dramatically in Iowa, as in the rest of the country, since the 1990s—more than 270% between 1991 and 2020 as seen in figure 9. While measures of health expenditures do not distinguish between the price of goods and the utilization of the goods (i.e. the quantity of healthcare consumed), these increases in health expenditure in the U.S. have primarily been due to the increase in prices as opposed to an increase in utilization.[xxx] Therefore, they give an estimate of the changes in the cost of healthcare. In context, the Consumer Price Index increased by only 92% during this period, well below the 270% increase in healthcare expenditures.

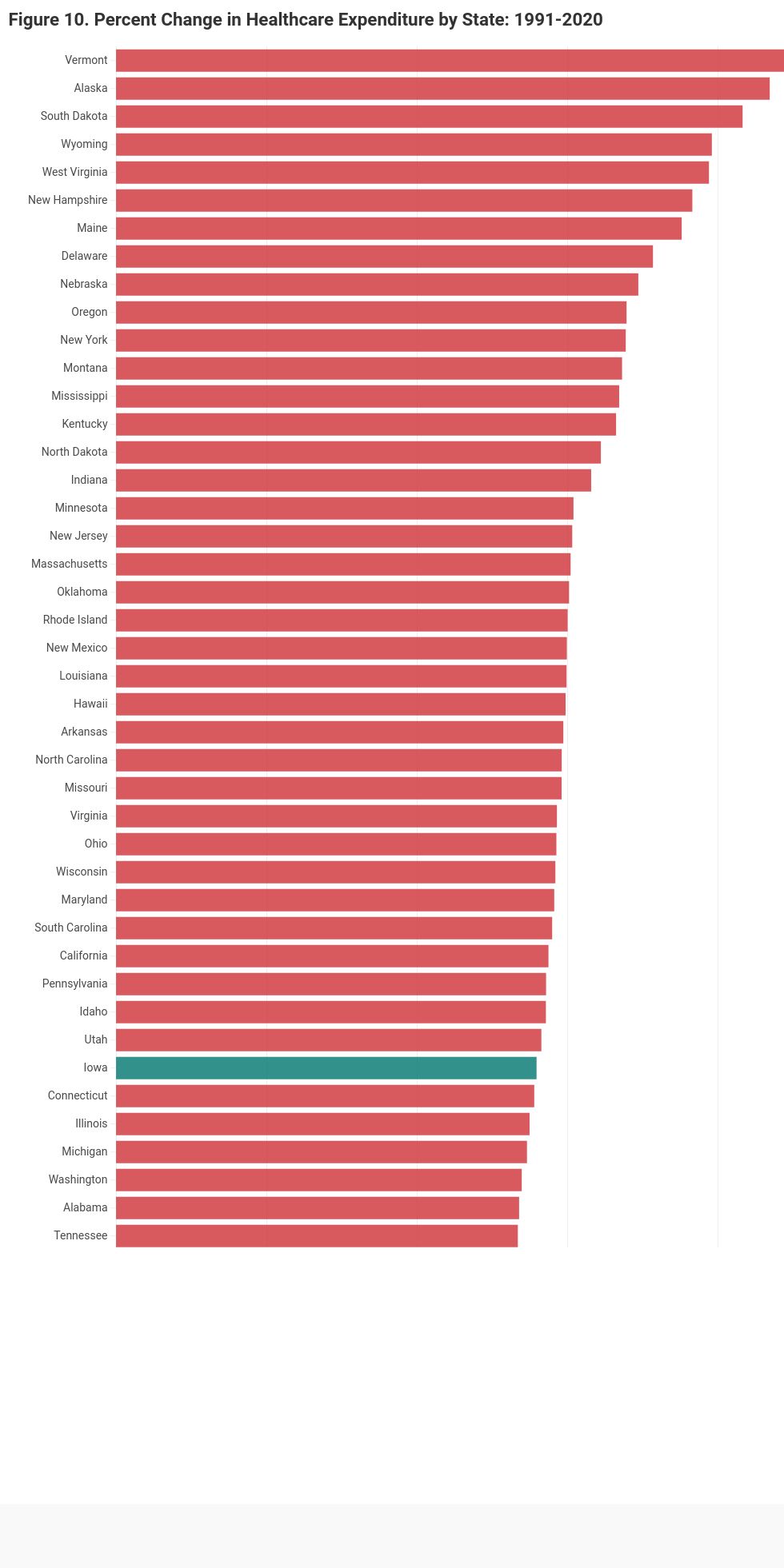

Figure 9 also shows the percent change in expenditure by healthcare category. In Iowa, the largest increase in health expenditures has been in home healthcare, with an increase of 456%. Expenditures on prescription drugs increased by 300% between 1991 and 2010 but have remained relatively constant between 2010 and 2020. The total increase in health expenditures for Iowans (280%) is below the average increase in health expenditures seen across the country during this period (306%) as depicted in figure 10. While healthcare expenditures are rising for Iowans, they are not rising as fast as healthcare expenditures in the rest of the country. Further research should investigate the mechanisms for these differences in increased rates of healthcare expenditures.

Iowa and the United States have seen a clear and consistent upward trend in healthcare expenditures. The causes are complex, multifaceted, and hotly disputed. However, solutions can come from one of two approaches as understood from an economic perspective. Either decrease prices or improve health through preventative measures. More research is needed to evaluate the effectiveness of state policy strategies in Iowa, such as enhancing competition and price transparency, in controlling healthcare prices.

[xxxi] In the meantime, reducing the need for medical care by improving health can decrease subsequent medical expenditures.

The U.S. spends 90% of its total healthcare budget to care for individuals with chronic and mental health conditions, including heart disease, stroke, cancer, diabetes, obesity, arthritis, Alzheimer’s disease, epilepsy, and tooth decay.

[xxxii] Further, over 50% of Iowans over the age of 18 have been diagnosed with multiple chronic conditions—many of which can be improved through lifestyle changes, nutrition, and professional medical support.

[xxxiii] Further research should focus on how policies can promote preventative health measures in Iowa and decrease the disease burden on the population and the healthcare system.

Iowa has the 7th highest insurance coverage nationally.

Health insurance is the central way individuals pay for healthcare. Insurance in the United States comes primarily through government-funded Medicare and Medicaid and through private health insurance (PHI) provided by employers or the private market. Figure 11 shows the total expenditures in Iowa financed by insurance type: private health insurers (PHI), Medicare, and Medicaid.

In 2019, PHI funded 36% ($10.5 billion) of healthcare expenses in Iowa, Medicare funded 23% ($6.8 billion), and Medicaid 16% ($4.7 billion).

[xxxiv] The percentage of total health expenditures in Iowa financed through Medicare increased from 17% in 2001 to 23% by 2019, a 35% increase. In the rest of the country over the same period, Medicare spending increased from 19% of total healthcare spending to 23% of total healthcare spending, an increase of 23%. The percent of total health expenditures financed through Medicaid in Iowa increased from 12% in 2001 to 16% in 2019, an increase of 35%. Over the same period, the percent of expenditures financed through Medicaid in the US only increased by 5% to 17% of the total. In 2001, Iowa financed a smaller amount of total health expenditures through Medicaid and Medicare than the average state in the country. By 2019, it financed about the same amount of health expenditures through public insurance as the average state in the country. While the state has become no more dependent on public insurance than the rest of the country, its reliance on public insurance increased significantly relative to where it was in 2001.

It is worth noting that the prices paid by PHI and public insurance for the same procedures vary substantially. A 2022 Congressional Budget Office report estimated that, in Iowa, Medicare pays hospitals at an average rate of 92% of the national average price paid by Medicare fee for service (FFS).

[xxxv] In other words, Medicare reimburses hospitals in Iowa at a rate 8% lower than the average hospital in the United States. Commercial health insurers pay much higher prices.

[xxxvi] In Iowa, commercial insurers pay average prices that are 263% higher than the national average Medicare FFS. While the commercial price paid to hospitals varies by state from 187% to 318% of the Medicare FFS national average, the average across the country is 236%, slightly lower than that seen in Iowa. Related trends are seen for physician prices, where physician services in Iowa are reimbursed by Medicare at a rate of 95% of the national average Medicare FFS. Commercial insurers pay a price for physician services that is 144% of the Medicare FFS national average, which is 10

th highest by state for physician prices in the country.

[xxxvii] Large gaps in reimbursement rates between public and private insurance can potentially lead to differences in access and quality of care for patients under each type of insurance. In addition, these gaps can place a larger financial burden on those financing private insurance, as providers may increase prices for private insurers while public reimbursements remain relatively stagnant.

The financing of health expenditures describes how the aggregate health expenses in the state are paid for but does little to describe the rates of insurance among the population. Between 2013-2022, the rate of employer-sponsored health insurance decreased slightly from 60.2% of the population of Iowa to 59.5%; rates of Medicare enrollment increased from 16.9% to 19.4%; rates of Medicaid enrollment increased from 16.3% to 19.8%; rates of direct insurance (private insurance that is not employer-sponsored such as the private market through healthcare.gov) decreased from 16.5% to 16.1%; and the uninsured rate decreased from 8.1% to 4.5%.

[xxxviii] These rates as a percent change from 2013 are shown in figure 12.

The large decrease in the uninsured rate occurred between 2013 and 2015 due to the Affordable Care Act. Indeed, even after the repeal of the Individual Mandate, the rate of uninsured in Iowa has remained consistently low. At 4.5% in 2022, the state has the 7

th lowest uninsurance rate by state in the US, as seen in figure 13, while rates of public insurance in Iowa are similar to the average rate in the US. Thus, financial access to healthcare through insurance is a strength of Iowa.

However, as insurance coverage has increased, so have costs. Rising costs for healthcare have in turn pushed up the cost of obtaining private insurance. As discussed previously, healthcare expenditures in Iowa increased by 33% between 2009 and 2022 from $6,889 to $9,193 per capita.

[xxxix] Meanwhile, the average yearly cost of health insurance—including contributions from employers and employees—has increased 67% from $4,453 to $7,433 during this same time for a single plan.

[xl] The average yearly cost for a family plan in 2022 was $12,036. Employees, on average, contributed $1,845 and $3,184, respectively, for these single and family plans.

[xli]

As seen in figure 14, the total cost of a single health insurance plan, including the employee and employer contribution, rose 67% between 2009 and 2022. However, the employee contribution to a single plan increased by 115%. The total deductible for a single plan, another piece of health insurance that is paid by employees, increased by 106%. Put simply, health insurance is getting more expensive, and employees in Iowa are paying a higher portion of those costs. Specifically, the percent of total premiums that employees pay has increased from 19% to 25% during this time, an increase of 32%.

[xlii]

While total insurance premiums rose across the country at a similar rate during this time, the average employee contribution across all states rose by only 71%, compared to 115% in Iowa. In addition, average out-of-pocket maximums for Iowans have increased from $3,501 in 2016 to $4,345 in 2022—an increase of 24%.

[xliii] As of 2022, Iowans have the fourth largest percent employee contribution (25%) to employer sponsored health insurance of any state.

[xliv]

While health expenditures in Iowa increased by more than 250% between 1990 and 2020, Iowans spend less than the national average. The percent of health expenditures financed through public insurance increased between 2001 and 2019 and is now close to that of the national average. Iowa has the 7

th lowest uninsurance rate while rates of public insurance are similar to the national average. As health insurance becomes more costly, employees in Iowa are financing a larger part of the increased cost of health insurance. Further research could explore the impact of rising healthcare and insurance costs on Iowa employers. Although employees bear a significant portion of the increased insurance costs, employers also face higher expenses. Recent studies suggest that rising healthcare costs reduce overall income and employment in non-health sectors due to the cost of providing employer-sponsored health insurance.

[xlv] This trend could disproportionately affect smaller local businesses with tighter operating margins. More research could illuminate specific impacts on Iowa employers.

Iowa’s Rural Healthcare Landscape

Iowa faces substantial challenges in providing adequate healthcare to its rural residents. Access to healthcare providers in these areas is often limited, leaving residents with less accessibility to timely and appropriate medical care from primary care physicians, OBGYNs, and other medical professionals. Rural providers are also much more likely to operate at a loss, leaving residents with greater risk of hospital and clinic closures. These closures further exacerbate the difficulty of obtaining necessary medical services by forcing residents to travel longer distances for care, or in some cases, to go without it altogether.

Consequently, these factors have led to disparities in health outcomes between rural and urban regions of the state. Trends among rural communities signal worrying rates of health issues, which ultimately lead to high rates of premature death. The obesity rate is 36.8% for urban counties and 38.4% for rural counties; diabetes prevalence is 8.3% for urban counties and 8.9% for rural counties; and life expectancy is one year lower in rural counties (77.8 opposed to 78.8).

[xlvi] Additionally, more people in rural counties report frequent physical distress (9.1% vs 8.4%) and frequent mental distress (14.2% vs 13.6%) than in urban counties. These factors imply rural Iowans are at greater risk of health complications than the average urban Iowan.

This section delves into the current state of rural healthcare in Iowa, examining the availability of healthcare providers and the prevailing health trends affecting these communities. Understanding these factors is crucial for developing targeted strategies to improve healthcare access and outcomes for Iowa's rural population.

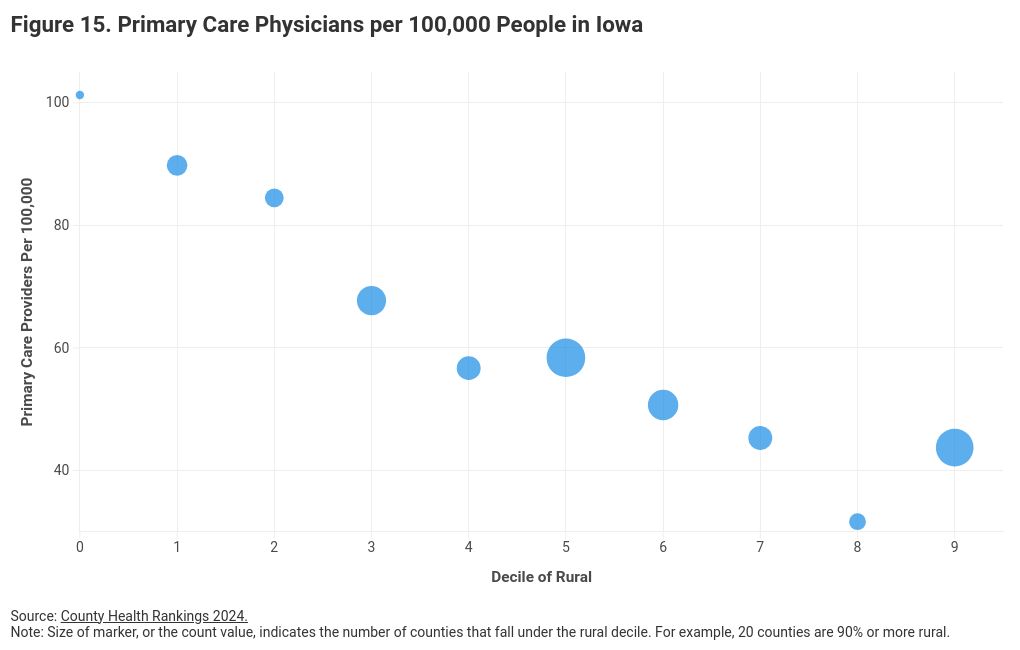

Iowa has 17% fewer physicians per capita in rural areas versus urban.

Primary care physicians in Iowa are an integral part of everyday health. While Iowa has a relatively strong supply of primary care physicians, rural communities face greater barriers to accessing healthcare than urban ones, leaving them at greater risk of worse health outcomes. The number of primary care physicians per 100,000 people serves as a top indicator for accessibility to care. Between 2013 and 2024, the physician ratio in Iowa decreased by 8% (from 55.3 to 51.4) for rural counties while it only decreased 1% (from 62.9 to 62.2) for urban counties.

[xlvii] Figure 15 illustrates the relationship between the percent of the county living in a rural area and the physician ratio. As this figure indicates, the more rural a county, the fewer primary care providers per 100,000 people. In counties where more than 90% of the population lives in a rural area, there are 43 primary care physicians per 100,000 people. By contrast, in counties where less than 20% of the population lives in a rural area, there are more than 90. In context, the average number of primary care physicians per 100,000 people across the U.S. is 63. Insufficient access to physicians can significantly decrease quality of life for rural Iowans.

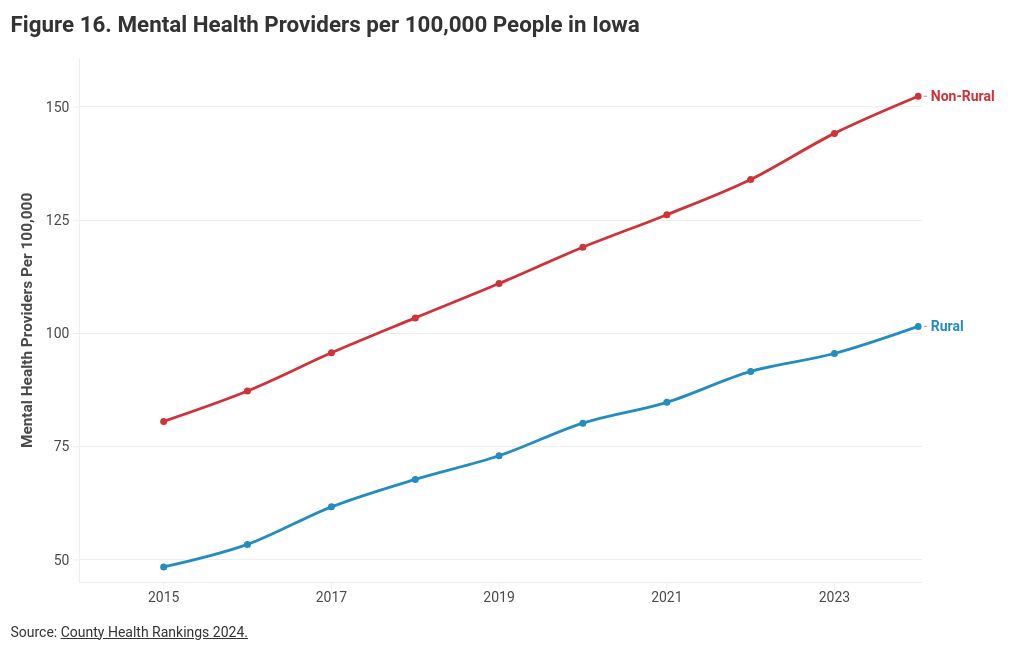

Access to mental health care has become a pressing issue across the United States. Some states have grappled with this nationwide mental health crisis by increasing accessibility to mental health care facilities to meet demand. Since 2015, the number of mental health providers per 100,000 people in Iowa has increased by 98% (48.4 per 100,000 to 95.6) for rural counties and 78% (80.6 per 100,000 to 144.2) for urban counties as seen in figure 16. This is an incredible accomplishment in the state. This lays in contrast, however, to the significant increase in mental health facility closures illustrated in the Business Climate and Outlook section of this report. The mental health facility closures include locations such as Community Mental Health Centers, Residential Care Facilities for the Intellectually Disabled, Subacute Mental Health Facilities, and Intermediate Care Facilities for Individuals with Intellectual Disabilities. These care facilities support individuals with more intense mental health struggles. In short, Iowa has significantly increased the number of mental health providers available in the state, but the number of intensive, mental health focused facilities has decreased. Although provider growth in rural counties has outpaced that of urban ones, a disparity persists between the two.

Iowa’s urban-rural provider disparity underscores the ongoing challenges rural communities face in accessing mental health care. Despite the efforts to improve, the state still lacks an adequate level of mental healthcare to rural communities, directly impacting the lives of many Iowans. Individuals in these rural communities are more likely to experience untreated mental health conditions, which can contribute to higher rates of depression, anxiety, and more. Addressing this gap is essential for breaking cycles of mental health illness and improving the well-being of rural communities.

[xlviii]

Another gap between provider access for rural and urban communities in Iowa comes in the form of maternal care, a type of healthcare essential for guaranteeing the well-being and health of mothers and their infants. Iowa relies on its families to thrive, as they are the backbone of rural communities all over the state. Ensuring accessible maternity care is essential for supporting these families, fostering healthy child development, and maintaining the populations of Iowa’s rural regions. Most rural births are overseen by family physicians, further illustrating the importance of these family providers. However, the data illustrated in this report suggests a trend of new practitioners moving away from family physicians into nurse practitioner roles, which is a potential concern for maternal care as nurse practitioners can provide prenatal care but are not licensed to deliver babies. While there are an increasing number of nurse midwives in the state which may help bridge the rural divide in maternal care, these providers are not necessarily located in the most high-need areas. Without a steady supply of proper healthcare professionals, prospective parents are left with the burden of uncertainty about whether raising a family is medically safe.

Additionally, 62 of Iowa’s 77 rural counties (and 9 of the urban counties) do not have a practicing OBGYN as illustrated in figure 17. Of the rural counties with a practicing OBGYN, these providers are significantly older; the average number of years since medical school graduation (a proxy for age) is 20 for OBGYNs in urban counties in comparison to 25 for OBGYNs in rural counties.

[xlix] Rural communities face a worrisome shortage of OBGYN providers. Even counties with providers struggle with keeping up with demand, given that older workforces suggest earlier retirements—as discussed in the workforce section of “Business Climate and Outlook.” This implies that in the coming years, existing providers may also struggle to secure replacements for these professionals critical to Iowa’s healthcare system.

Healthcare facility closures have been a recent issue throughout the United States and have been especially prevalent across rural regions. In Iowa, however, there have been a similar number of healthcare facility closures in rural and urban counties between 2008-2023.

[l] When it comes to understanding the financial burden of hospitals in rural areas, it is helpful to investigate differences in operating margins between hospitals in rural and urban areas. Based on data from the Iowa Hospital Association, there is a small but significant correlation between hospital operating profits as a percent of revenue and population of the county, indicating that hospitals in counties with small populations are more likely to struggle financially. The average operating profit as a percent of revenue tends to be higher for hospitals in counties with larger populations.

[li] [lii]For example, in 2019, hospitals in counties with more than 75,000 people (the top 10 largest counties in Iowa) had an average profit as a percent of revenue of 2.6%, whereas counties with fewer than 75,000 people had an average profit as a percent of revenue of -1.0%. This is concerning for rural Iowa as hospitals are likely to cut services when faced with financial pressures.

Rural Iowa’s older population strains healthcare providers.

America’s population is aging, and Iowa is no exception. Due to higher life expectancy and lower fertility rates, the percentage of the population over 65 in Iowa has been steadily increasing, outside of a brief drop due to Covid as seen in figure 18. Urban populations are aging at a slightly higher rate than rural ones, but approximately 5% more of the population in rural counties are over age 65 than in urban counties. The aging nature of the population explains some of why Iowans spend more per capita on nursing homes and home health, as found in the “Expenditures and Insurance” section. However, Iowa spends the 6

th highest amount of any state on nursing homes but ranks 20

th in the nation for the age of the population. This indicates that Iowans spend a relatively large amount of healthcare expenses per capita on the aging population, even when controlling for the number of aging individuals.

An aging population puts further strain on the healthcare system, as demand for health services increases with age. This is illustrated by the fact that those 65 and older make up 18% of the population but accrue more than a third of total healthcare expenditures.

[liii] Additionally, healthcare expenditures in the last three years of life are estimated to account for more than 15% of lifetime health spending.

[liv] While both urban and rural communities are facing the additional strain of an aging population on the healthcare system, the aging gap is slowly shrinking potentially due to an increase in the rate of premature deaths in rural counties.

[lv]

Premature deaths have increased in Iowa in both rural and urban counties since 2015. Premature deaths measure the years of potential life lost before age 75 per 100,000, emphasizing earlier deaths that might have been prevented.

[lvi] The rate of premature deaths in 2024 remains higher in rural counties at 377 per 100,000 (an increase of 18% since 2015) than in urban counties at 340 per 100,000 (an increase of 9% since 2015).

[lvii] The county-level premature death rate in Iowa in 2024 ranged from 184 to 469 per 100,000. High rates of premature deaths create extra stress on healthcare institutions, especially in regions without adequate preventative services. Resources are allocated away from preventative care towards emergency care, leaving Iowa’s already weak rural healthcare system struggling to nurse a healthier population. There is also a stark geographic distribution of premature deaths, with higher rates in the south and west parts of the state, areas farther away from major cities, as seen in figure 19.

While premature deaths are caused by a variety of factors, drug overdoses are one of those potential factors. As documented in CSI Iowa’s 2024 report,

Iowa in the Context of America’s Fentanyl Epidemic, deaths from synthetic opioid overdoses in Iowa increased from 0.96 in 100,000 in 2015 to 6.4 in 100,000 in 2023.

[lviii] Treating drug overdoses can become especially difficult when there are fewer options or when traveling longer distances, leaving rural Iowans more prone to overdose fatalities. However, more research needs to be done on the geographic distribution of these overdose deaths and whether they are related to the heightened premature death rate in rural areas.

The data clearly show Iowa’s rural communities have less access to healthcare providers, particularly primary care physicians and OBGYNs. Hospital financial data suggest a small relationship between hospital profit margins and county population, which may contribute to provider or service deficiencies in rural counties. The challenges are compounded by the fact that rural counties on average have older populations and higher rates of premature death, obesity, diabetes, and self-reported mental and physical health. It is therefore imperative to continue supporting the healthcare system in these disadvantaged communities. Solutions resolving demographic health trends, demand for healthcare professionals, and facilities facing financial instability are key to creating a more accessible healthcare system for rural communities.

Recent Public Policy Changes

This report surveys Iowa’s healthcare landscape, highlighting some of its greatest challenges: financial struggles leading to closures of healthcare facilities; significant increases in personnel vacancies; rising healthcare and insurance costs; and disparities in access to specialized care and health outcomes between rural and urban regions. Despite these concerns, Iowa still fares much better than the rest of the nation, ranking #2 in CSI’s healthcare competitive index. When considering the entirety of the United States, Iowa has been relatively successful in fostering improved infrastructure, enhancing healthcare access, and promoting economic growth. Iowa may continue to face challenges amidst a complex underlying United States healthcare system, but the state has taken many steps to improve Iowa’s healthcare landscape where state-level policy can make a difference.

Policymakers have worked with Iowans and providers to better understand the state’s healthcare challenges, which this report illuminates through data. Over the past several years, they enacted legislative measures to address many of those challenges. These measures seek to ensure every Iowan has access to the healthcare services they need regardless of where they live. Specifically, they aim to remove unnecessary and burdensome regulations, address funding shortages, and enhance the state’s efforts in recruiting and retaining healthcare providers. In some cases, they redesign aspects of the state’s healthcare system entirely.

Business of Health Care:

- The Iowa Legislature capped non-economic damage awards in medical malpractice cases to protect and improve Iowans’ access to health care services. (2023)[lix]

- The Iowa Legislature established rural emergency hospitals as a new hospital license category. (2023)[lx]

Workforce:

- The Iowa Legislature improved state behavioral health, disability, and addictive disorder services and programs, and transferred disability services to the Division of Aging and Disability Services of the Department of Human Services. (2024)[lxi]

- The Iowa Legislature passed a Family Medicine OB Fellowship program that provides obstetrical training to up to 4 physicians per year in exchange for practicing in a rural community for a minimum of 5 years. (2023)[lxii]

- The Iowa Legislature passed a bill that prohibited the use of non-compete clauses in mental health professionals’ employment contracts to maintain continuity of care for patients and improve access. (2023)[lxiii]

- The Iowa Legislature established the Iowa Office of Apprenticeship to oversee, expand, and promote apprenticeship programs at the state level to build Iowa’s workforce. (2023)[lxiv]

- The Iowa Legislature expanded employment eligibility and work-based learning opportunities for young Iowans seeking to gain experience in the workforce. (2023)[lxv]

- The Iowa Legislature established a Mental Health Professional loan repayment program. (2022)[lxvi]

- The Iowa Legislature funded additional positions in the University of Iowa Psychiatric Residency Program. (2022)[lxvii]

- The Iowa Legislature funded additional pathways and removes barriers to professional licensure in the state. The bill allows new Iowa residents with an out-of-state license to use their skills and training in the same licensed profession, recognizes three years of work experience as a substitute for any education, training and work experience requirements, waives initial licensing fees for first-time applicants of families earning less than 200 percent of the FPL, and creates a uniform standard of review for denial of licensure based on a person’s conviction history. (2020)[lxviii]

Workforce – Regulatory Burdens:

- The Iowa Legislature allowed Iowa to join the dental and dental hygienist interstate licensure compact to reduce barriers to license portability across state lines. (2023)[lxix]

- The Iowa Legislature removed the requirement that a physician assistant practices under supervision after two years. (2023)[lxx]

- The Iowa Legislature removed one-year out-of-state licensure requirements for universal license recognition, removed residency requirements for universal recognition for most professions, offered temporary licensure for military spouses if they don’t qualify for universal license recognition, and created a work-based learning program supervisor for students to receive credit. (2022)[lxxi]

Workforce – Childcare

- The Iowa Legislature opened additional childcare slots by establishing new minimum child-to-staff ratios in childcare centers of 1:7 for children aged 2, and 1:10 for children aged 3. The bill also addressed workforce challenges by allowing childcare center employees 16 and older to work without additional supervision. (2022)[lxxii]

- The Iowa Legislature passed a bill that incentivized child-care providers to accept more Child Care Assistance (CCA) families by allowing parents to pay the difference between CCA and private rates. (2022)[lxxiii]

Insurance Coverage & Costs:

- The Iowa Legislature passed an Act to improve insurance coverage for biomarker testing, which assists in cancer treatment. (2024)[lxxiv]

- The Iowa Legislature passed an Act to improve insurance coverage for supplemental and diagnostic breast examinations. (2024)[lxxv]

Behavioral Health:

- The Iowa Legislature directed the Department of Health Services to establish tiered in-patient payment rates in the Medicaid program for acute mental health services. (2022)[lxxvi]

- The Iowa Legislature designated schools as a site of service for mental health providers, allowing schools to contract with mental health professionals and bill insurance. (2020)[lxxvii]

- Through executive order, Iowa established a children’s behavioral health system, which has since led to passed legislation and annual reforms to improve access to behavioral health services. (2018)[lxxviii]

Maternal Health:

- The Iowa Legislature extended post-partum Medicaid coverage for new mothers, ensuring that new mothers and their babies have access to the care they need in the year following a delivery. (2024)[lxxix]

- The Iowa Legislature passed a program (MOMs) that was designed to improve access for pregnant women and new mothers to pregnancy resource centers. (2022)[lxxx]

New policies take time—sometimes years—to implement. Once fully implemented, it can take several more years for them to work their effect on the healthcare marketplace. Additionally, data releases often lag the event the data measures by a year or more. If recent policy changes listed in this section have their intended effect, the new trends that demonstrate their effectiveness may not appear in the data for several years. With the data available today, this report cannot yet draw correlations between recent policy changes and outcomes with any degree of confidence. However, the data points surveyed in this report, once updated with future years’ data, can serve as a starting point for such an evaluation.

Conclusion

The U.S. healthcare economy faces a complex landscape marked by increasing costs, workforce shortages, high disease burdens, and inequitable access to care. While Iowa contends with these challenges, it performs well relative to other states. For example, CSI’s Healthcare Competitiveness Index ranks Iowa second in the nation, US News ranks Iowa 9th in the nation for healthcare access and 21st for overall healthcare, and the Agency for Healthcare Research and Quality places Iowa in the top 10 states for overall quality of healthcare.[lxxxi] Even though Iowa continues to be a leader in healthcare in many ways relative to the rest of the country, it is important to understand the real challenges that Iowans face on an absolute level.

Despite its strong performance, Iowa faces significant hurdles. Though 5% lower than the national average, 45% of Iowa hospitals operated at a loss in 2022. The increased number of hospitals operating at a loss is driven primarily by increases in operating costs for these businesses, a symptom of rising input costs and administrative burdens in an increasingly complex regulatory regime. Between 2008 and 2023, more healthcare facilities closed than opened, with mental health centers, elderly care, and home health facilities being most affected. While Iowa’s healthcare workforce is robust, ongoing recruitment is essential to replace an aging workforce.

Healthcare costs and insurance premiums have surged across the country, and Iowa is no exception. From 2009 to 2022, healthcare expenditures in Iowa increased by 33% and health insurance costs by 67%, slightly lower than national trends. However, employee contributions to employer-sponsored insurance in Iowa increased by 115%, compared to the national average of 71%. In 2001, Iowa financed a smaller amount of total health expenditures through public insurance than the average state in the country, but by 2019 it financed about the same as the national average. As of 2022, only 4.5% of Iowans were uninsured, ranking Iowa 7th lowest in the nation. This is a channel through which Iowans have increased financial access to care compared to the rest of the country.

Rural Iowa faces unique challenges in healthcare access and outcomes. Although Iowa ranks highly for physician access, rural counties have 17% fewer physicians per capita than urban areas. The state has increased mental health provider availability since 2015, yet rural areas still lag urban areas. Maternal care access is also substantially lower in these urban counties, as it is in rural areas across the country. Additionally, Iowa's aging population, particularly concentrated in rural areas, imposes a heavier burden on the healthcare system. Rural areas are experiencing a concerning rise in preventable and premature deaths across the country as well as in Iowa. Despite its challenges, Iowa maintains a competitive healthcare industry with relatively strong access to care through insurance and provider availability.

While Iowa’s healthcare system faces substantial challenges, these are not unique to the state. Variables outside of the control of state policymakers such as federal laws and regulations have largely induced challenges common across all states. Nonetheless, Iowa policymakers have made meaningful efforts to improve outcomes where state-level policies may do so. As new data becomes available, this report may serve as a marker for evaluating their effectiveness. It may also help public- and private-sector decision makers identify where additional reforms could improve the state’s healthcare system. Finally, the report may serve as a springboard for future research

[i] National Health Expenditures 2022 Highlights, prepared by the U.S. Centers for Medicare & Medicaid Services (Baltimore, 2022), https://www.cms.gov/files/document/highlights.pdf.

[ii] Office of the Attorney General, “For Older Iowans,” Iowa Department of Justice, https://www.iowaattorneygeneral.gov/for-consumers/for-older-iowans#:~:text=Iowa%20is%20an%20aging%20state,population%20age%2075%20or%20older.

[iii] USDA Economic Research Service, “Rural-Urban Continuum Codes,” U.S. Department of Agriculture, last modified January 22, 2024, https://www.ers.usda.gov/data-products/rural-urban-continuum-codes/.

[iv] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” University of Wisconsin Population Health Institute (2024), https://www.countyhealthrankings.org/health-data/iowa?year=2024.

[v] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024.

[vi] Steven L. Byers, “Colorado’s 2023 Economic Performance Index,” Common Sense Institute (February 2024), https://commonsenseinstituteco.org/colorados-2023-economic-performance-index.

[vii] U.S. Bureau of Economic Analysis, “SASUMMARY State annual summary statistics: personal income, GDP, consumer spending, price index, and employment,” U.S. Department of Commerce, 2024, https://apps.bea.gov/itable/?ReqID=70&step=1&_gl=1*19j0sol*_ga*MTYzOTAyMzUxNi4xNzIxMjM2ODI3*_ga_J4698JNNFT*MTcyMTIzNjgyNy4xLjAuMTcyMTIzNjgyNy42MC4wLjA.#eyJhcHBpZCI6NzAsInN0ZXBzIjpbMSwyOSwyNSwzMSwyNiwyNywzMF0sImRhdGEiOltbIlRhYmxlSWQiLCI2MDAiXSxbIk1ham9yX0F.

[viii] Regional Economic Models Inc. (REMI), REMI PI+ Model, Version 3.2 (2024).

[ix] REMI.

[x] Health Resources & Services Administration Data Warehouse (updated 2023), https://data.hrsa.gov.

[xi] Iowa Open Data, (object name Insurance Companies Licensed in Iowa, updated 2024), https://data.iowa.gov/Regulation/Insurance-Companies-Licensed-in-Iowa/tzrk-47xh/data.

[xii] Kaiser Family Foundation, “Market Share and Enrollment of Largest Three Insurers – Large Group Market (2021),” https://www.kff.org/other/state-indicator/market-share-and-enrollment-of-largest-three-insurers-large-group-market/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D; Wellmark Blue Cross and Blue Shield, https://www.wellmark.com/

[xiii] American Hospital Association, “America’s Hospitals and Health Systems Continue to Face Escalating Operational Costs and Economic Pressures as They Care for Patients and Communities,” Costs of Caring (May 2024), https://www.aha.org/costsofcaring#:~:text=While%20recent%20data%20suggest%20that,1.

[xiv] Iowa Hospital Data, prepared by the Iowa Hospital Association (2022), https://www.iowahospitalfacts.com.

[xv] American Hospital Association, “Massive Growth in Expenses & Rising Inflation Fuel Financial Challenges for America’s Hospitals & Health Systems,” American Hospital Association (2022), https://www.aha.org/guidesreports/2022-04-22-massive-growth-expenses-and-rising-inflation-fuel-continued-financial.

[xvi] Office of Inspector General, Hospital’s Compliance with the Provider Relief Fund Balance Billing Requirement for Out-of-Network Patients, U.S. Department of Health and Human Services (2021), https://oig.hhs.gov/reports-and-publications/workplan/summary/wp-summary-0000647.asp#:~:text=The%20Coronavirus%20Aid%2C%20Relief%2C%20and,and%20other%20health%20care%20providers.

[xvii] These numbers exclude VA/Other hospitals.

[xviii] CAQH, “2023 CAQH Index Report,” CAQH Insights (2023). https://www.caqh.org/hubfs/43908627/drupal/2024-01/2023_CAQH_Index_Report.pdf.

[xix] Direct Care Worker Registry & Health Facility Database of the Iowa Department of Inspections & Appeals, https://dia-hfd.iowa.gov/. Facilities included in the Iowa Department of Inspections and Appeals (DIA) data include: ambulatory surgical centers, assisted living facilities, dialysis facilities, elderly group homes, home health agencies, hospices, hospitals, intermediate care facilities for individuals with an intellectual disability, intermediate care facilities for persons with mental illness, nursing facilities and skilled nursing facilities, and residential care facilities. These facilities require licensing, certifications, and inspections that DIAL has oversight for. DIAL conducts inspections of these facilities and helps them get to compliance. Facilities not included in this dataset do not have the same compliance standards, so they are not in the DIAL jurisdiction. These facilities include family practice, acupuncture, and chiropractic, among others. Health care employment agencies were excluded from the analysis.

[xx] Specifically using the IDIA “Entity Types”, we define elderly care as: Assisted Living Programs, Assisted Living Programs for People with Dementia, Elder Group Homes, Free Standing NF, Free Standing NF/SNF, HSP-NF, HSP-SNF, HSP-SNF/NF, Residential Care Facilities, and Adult Day Services.

[xxi] American Health Care Association, “Access to Care Report,” American Health Care Association (August 2023), https://www.ahcancal.org/News-and-Communications/Fact-Sheets/FactSheets/Access%20to%20Care%20Report%20August%202023.pdf .

[xxii] Direct Care Worker Registry & Health Facility Database of the Iowa Department of Inspections & Appeals, https://dia-hfd.iowa.gov/.

[xxiii] The full list of IDIA “Entity Types” included here as mental health centers are Community Mental Health Centers, Residential Care Facilities for the Intellectually Disabled, Residential Care Facilities for Persons with Mental Illness, Subacute Mental Health Facilities, Intermediate Care Facilities for Individuals with Intellectual Disabilities, Psychiatric Medical Institutions for Children, and HSP-PSY, RCF 3-5 Bed ID/MI/DD/BI.

[xxiv] Other facilities not included in this analysis are ambulatory surgical centers, portable x-ray services, and transplant centers.

[xxv] Direct Care Worker Registry & Health Facility Database of the Iowa Department of Inspections & Appeals, https://dia-hfd.iowa.gov/; Kaiser Family Foundation, “State Health Facts: Total Hospital Beds,” 2023, https://www.kff.org/other/state-indicator/total-hospital-beds/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D\. Data includes staffed beds for community hospitals.

[xxvi] Center for Healthcare Quality & Payment Reform, “Rural Hospitals at Risk of Closing (2024),” https://ruralhospitals.chqpr.org/downloads/Rural_Hospitals_at_Risk_of_Closing.pdf.

[xxvii] Office of Inspector General, “Hospital’s Compliance,” https://oig.hhs.gov/reports-and-publications/workplan/summary/wp-summary-0000647.asp#:~:text=The%20Coronavirus%20Aid%2C%20Relief%2C%20and,and%20other%20health%20care%20providers.

[xxviii] National Downloadable File of the Centers for Medicare & Medicaid Services, https://data.cms.gov/provider-data/dataset/mj5m-pzi6. Providers are categorized based on their self-reported primary medical specialty.

[xxix] Mercer, “US Healthcare Labor Market,” Mercer (2021), https://www.mercer.com/content/dam/mercer/assets/content-images/north-america/united-states/us-healthcare-news/us-2021-healthcare-labor-market-whitepaper.pdf.

[xxx] Uwe E. Reinhardt, Priced Out: The Economic and Ethical Costs of American Health Care (Princeton University Press: 2019). Analysis on the breakdown of cost versus utilization is out of the scope of this report, but an important area for future research.

[xxxi] See the section in this report entitled “Recent Public Policy Changes” for a survey of some of these state policy changes.

[xxxii] Center for Disease Control, “Fast Facts: Health and Economic Costs of Chronic Conditions,” Chronic Disease (2024). https://www.cdc.gov/chronic-disease/data-research/facts-stats/index.html#:~:text=The%20impact%20of%20chronic%20diseases,chronic%20and%20mental%20health%20conditions.

[xxxiii] Daniel Newman, Michelle Tong, Erica Levine, and Sandeep Kishore. "Prevalence of multiple chronic conditions by US state and territory, 2017." PLoS One 15, no. 5 (2020): e0232346.

[xxxiv] Health Expenditures by State of Residence, prepared by the Centers for Medicare & Medicaid Services, http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/resident-state-estimates.zip. The other 25% of expenditures were financed through out-of-pocket payments and other third-party payers, such as worker’s compensation, and public health activities. CMS does not provide data on the expenses paid by these parties by state.

[xxxv] The Prices that Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services, prepared by the Congressional Budget Office (2022), https://www.cbo.gov/system/files/2022-01/57422-medical-prices.pdf.

[xxxvi] Commercial insurers in this study were restricted to employer-sponsored health insurance plans which is a type of PHI.

[xxxvii] Christopher M. Whaley, Brian Briscombe, Rose Kerber, Brenna O’Neill, and Aaron Kofner, “Nationwide Evaluation of Health Care Prices Paid by Private Health Plans: Findings from Round 3 of an Employer-Led Transparency Initiative,” RAND (Santa Monica, CA: September 2020), https://www.rand.org/pubs/research_reports/RR4394.html.

[xxxviii] American Community Survey Tables for Health Insurance Coverage (2022), United States Census Bureau, https://www.census.gov/data/tables/time-series/demo/health-insurance/acs-hi.html.

[xxxix] National Downloadable File of the Centers for Medicare & Medicaid Services. https://data.cms.gov/provider-data/dataset/mj5m-pzi6.

[xl] Medical Expenditure Panel Survey Insurance Component, Agency for Healthcare Research and Quality (2022), https://datatools.ahrq.gov/meps-ic/?tab=private-sector-state&dash=26.

[xli] Medical Expenditure Panel Survey, Agency for Healthcare Research and Quality, https://meps.ahrq.gov/mepsweb/.

[xlii] These trends are similar for family plans, although prices of total premium, employee contribution and deductible have grown at similar rates to one another.

[xliii] Data on out of pocket maximums were not added to the Medical Expenditure Panel Survey until 2016.

[xliv] Medical Expenditure Panel Survey, Agency for Healthcare Research and Quality. https://meps.ahrq.gov/mepsweb/.

[xlv] Zarek Brot-Goldberg, Zack Cooper, Stuart V. Craig, Lev R. Klarnet, Ithai Lurie, Corbin L. Miller, “Who Pays for Rising Health Care Prices? Evidence from Hospital Mergers,” National Bureau of Economic Research (June 2024), https://www.nber.org/system/files/working_papers/w32613/w32613.pdf

[xlvi] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024.

[xlvii] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024.The average primary care physician rate by state in the country is 62.8 per 100,000.

[xlviii] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024.

[xlix] National Downloadable File of the Centers for Medicare & Medicaid Services. https://data.cms.gov/provider-data/dataset/mj5m-pzi6.

[l] Direct Care Worker Registry & Health Facility Database of the Iowa Department of Inspections & Appeals. https://dia-hfd.iowa.gov/.

[li] Iowa Hospital Data, prepared by the Iowa Hospital Association. https://www.ihaonline.org/information/databank/.

[lii] USDA Economic Research Service, “Rural-Urban Continuum Codes,” U.S. Department of Agriculture, https://www.ers.usda.gov/data-products/rural-urban-continuum-codes/.

[liii] Matthew McGough, Gary Claxton, Krutika Amin, and Cynthia Cox. ”How do health expenditures vary across the population?”. Peterson-KFF, Health System Tracker (2024), https://www.healthsystemtracker.org/chart-collection/health-expenditures-vary-across-population/#Share%20of%20total%20population%20and%20total%20health%20spending,%20by%20age%20group,%202021

[liv] French, Eric B., Jeremy McCauley, Maria Aragon, Pieter Bakx, Martin Chalkley, Stacey H. Chen, Bent J. Christensen et al. "End-of-life medical spending in last twelve months of life is lower than previously reported." Health Affairs 36, no. 7 (2017): 1211-1217.

[lv] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024.

[lvi] For example, a death at age 55 counts twice as much as a death at age 65, and a death at age 25 counts ten times as much as a death at age 70.

[lvii] County Health Rankings & Roadmaps 2024, “Iowa Data by County,” https://www.countyhealthrankings.org/health-data/iowa?year=2024. These numbers are calculated with moving averages so the increases post-2020 contain residual effects of the pandemic.

[lviii] Ben Murrey and Glenn Farley, “Iowa in the Context of America's Fentanyl Epidemic,” Common Sense Institute (June 26, 2024). https://commonsenseinstituteia.org/iowa-in-the-context-of-americas-fentanyl-epidemic/.

[lix] An Act Relating to Damage Awards Against Health Care Providers, Creating a Medical Error Task Force, and Including Effective Date and Applicability Provisions, HF 161, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%20161.

[lx] An Act Relating to Certain Health Facilities Including Ambulatory Surgical Centers and Rural Emergency Hospitals, Including Licensing Requirements and Fees, Providing Penalties and Making Penalties Applicable, Providing Emergency Rulemaking Authority, and Including Applicability and Effective Date Provisions, SF 75, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ba=SF+75&ga=90&utm_medium=email&utm_source=govdelivery.

[lxi] An Act Related to State Behavioral Health, Disability, and Addictive Disorder Services and Related Programs, Including the Transition of Behavioral Health Services from a Mental Health and Disability Services System to a Behabioral Health Service System, the Transfer of Disability Services to the Division of Aging and Disability Services of the Department of Health and Human Services, the Elimination of the Commission on Aging, the Elimination of Special Intellectual Disability Units at State Mental Health Institutes, Making Appropriations, and Including Effective Date Provisions, HF 2673, State of Iowa 90th General Assembly (2024). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%202673.

[lxii] An Act Relating to Appropriations for Veterans and Health and Human Services and Including Other Related Provisions and Appropriations Including Health Policy Oversight, Public Assistance Program Provisions and a Public Assistance Modernization Fund, Sprinkler Systems for Home and Community-Based Services Waiver Recipient Residences, a State-Funded Family Medicine Obstetrics Fellowship Program and Fund, Adoption Subsidy Program Nonrecurring Adoption Expenses, Real Estate Transactions Involving Departmental Institutions, Providing Penalties, and Including Effective Date and Other Applicability Date Provisions, SF 561, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=SF%20561 .

[lxiii] An Act Prohibiting Specified Provisions in Agreements Between Employers and Certain Mental Health Professionals and Including Effective Date Provisions, HF 93, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%2093.

[lxiv] An Act Relating to Apprenticeships and Establishing an Iowa Office of Apprenticeship and Iowa Apprenticeship Council, SF 318, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=SF%20318.

[lxv] An Act Relating to Youth Employment, Providing for a Minor Driver’s License Interim Study Committee, and Making Penalties Applicable, SF 542, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=SF%20542.

[lxvi] An Act Relating to the Establishment of a Mental Healtch Professional Loan Repayment Program Within the College Student Aid Commission, HF 2549, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=HF%202549.

[lxvii] An Act Relating to Appropriations for Health and Human Services and Veterans and Including Other Related Provisions and Appropriations, Providing Penalties, and Including Effective Date and Retroactive and Other Applicability Date Provisions, HF 2578, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=HF%202578.

[lxviii] An Act Relating to Governmental and Regulatory Matters Including the Granting and Renewal of Licenses, Certificates, and Registrations, and Including Effective Date Provisions, HF 2627, State of Iowa 88th General Assembly (2020). https://www.legis.iowa.gov/legislation/BillBook?ga=88&ba=HF%202627.

[lxix] An Act Establishing the Dentist and Dental Hygienist Compact, HF 656, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%20656.

[lxx] An Act Providing for the Collaborative Practice of Physician Assistants by Allowing for the Practice of Physician Assistants without Supervision by a Physician, HF 424, State of Iowa 90th General Assembly (2023). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%20424.

[lxxi] An Act Relating to Various Matters Under the Purview of the State, Including City and County Inspections, Work-Based Learning, Recruitment of Health Care Professionals, Regulations Affecting Veterans and Military Spouses, Insurance Producer Temporary Licenses, and Including Applicability Provisions, SF 2383, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=SF%202383.

[lxxii] An Act Relating to Child Care Center Minimum Age Requirements for Employees and Staff-to-Children Ratios, and Including Effective Date Provisions, HF 2198, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=HF%202198.

[lxxiii] An Act Relating to Payments to Child Care Providers from Families Participating in the State Child Care Assistance Program, HF 2127, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=HF%202127.

[lxxiv] An Act Relating to Insurance Coverage for Biomarker Testing, HF 2668, State of Iowa 90th General Assembly (2024). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%202668.

[lxxv] An Act Relating to Insurance Coverage for Supplemental and Diagnostic Breast Examinations, HF 2489, State of Iowa 90th General Assembly (2024). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=HF%202489.

[lxxvi] A Bill for an Act Relating to Reimbursement of Psychiatric Intensive Care Under the Medicaid Program, HF 2546, State of Iowa 89th General Assembly (2022). https://legiscan.com/IA/bill/HF2546/2021 .

[lxxvii] An Act Relating to the Provision of Behavioral Health Services Including via Telehealth in a School Setting, SF 2261, State of Iowa 88th General Assembly (2020). https://www.legis.iowa.gov/legislation/BillBook?ga=88&ba=SF%202261.

[lxxviii] Gov. Kim Reynolds, Exec. Order No. 2, State of Iowa Executive Department 2018. https://www.legis.iowa.gov/docs/publications/EO/966164.pdf.

[lxxix] An Act Relating to Eligibility for Pregnant Women and Infants Under the Medicaid Program, SF 2251, State of Iowa 90th General Assembly (2024). https://www.legis.iowa.gov/legislation/BillBook?ga=90&ba=SF%202251.

[lxxx] An Act Relating to Appropriations for Health and Human Services and Veterans and Including other Related Provisions and Appropriations, Providing Penalties, and Including Effective Date and Retroactive and Other Applicability Date Provisions, HF 2578, State of Iowa 89th General Assembly (2022). https://www.legis.iowa.gov/legislation/BillBook?ga=89&ba=HF%202578.

[lxxxi] U.S. News & World Report, under “Best States,” https://www.usnews.com/news/best-states/rankings/health-care; Agency for Healthcare Research and Quality, “Health Care Quality: How Does Your State Compare?,” https://www.ahrq.gov/data/infographics/state-compare-text.html.