Introduction

In terms of state budget competitiveness, Iowa is average but showing signs of improvement.

Between 2011 and 2021, the burden of state and local government in Iowa increased by every CSI metric. Debt increased, state spending grew faster than its GDP, and public employment growth outpaced population growth. However, the data in this report only goes through 2021. Some of the most aggressive policy changes enacted during the Reynolds administration that would improve Iowa’s state budget competitiveness do not show up in this report’s data.

This report affirms the need for policy reforms pursued in recent years by the governor, including tax reform and realignment of state government agencies.

Key Findings

- Iowa’s Competitiveness Index dropped from 79 in 2011 to 74 in 2021. An index value of 74 ranks Iowa 25th relative to 49 other states and the District of Columbia.

- Iowa’s Government Debt Service as a Percentage of Tax Revenue Competitiveness Index dropped slightly from 97 in 2011 to 95 in 2021.

- Iowa’s Government Spending as a Percentage of GDP Competitiveness Index decreased from 74 in 2011 to 70 in 2021.

- Iowa’s Government Employment as a Percentage of Population Competitiveness Index fell from 66 in 2011 to 57 in 2021.

- Iowa’s outstanding government debt increased 21.4% from $18.4B in 2011 to $22.3B in 2021.

- Iowa’s government spending increased 40.2% from $30.3B in 2011 to $42.5B in 2021.

- Recent policy reforms passed under the Reynolds administration since 2021—the last data year for this index—will likely improve Iowa’s state budget competitiveness in future years.

CSI’s Free Enterprise Report and State Budget Competitiveness Index

The Common Sense Institute issues a Free Enterprise Report annually. The report assesses each state’s competitiveness relative to 49 other states and the District of Columbia, and it provides data and analysis on eight policy areas: education, energy, healthcare, housing, infrastructure, public safety, Government budget, and taxes and fees. An increase (decrease) in an index indicates increased (decreased) competitiveness relative to the other 49 states and the District of Columbia. For example, if Iowa’s performance on a particular metric improves but other states improve by a greater amount, Iowa’s competitiveness rank relative to all states will decline. This report provides additional detail on the state budget competitiveness metric beyond what the Free Enterprise Report provides.

Government Budget Competitiveness Index

James Madison explained in The Federalist,

“The powers delegated by the proposed Constitution to the federal government are few and defined…. [T]he powers reserved to the several States will extend to all the objects which, in the ordinary course of affairs, concern the lives, liberties, and properties of the people, and the internal order, improvement, and prosperity of the State.” These reserved powers have generally been referred to as “police powers,” such as those required for public safety, health, and welfare. To exercise their reserved powers, states collect revenue from a variety of sources, issue debt, and develop budgets that allocate resources. To maintain a strong and healthy economy, states must practice sound budgeting and fiscal restraint while fulfilling their proper functions.

The Common Sense Institute has therefore developed a Government Budget Competitiveness Index for all 50 states and the District of Columbia to gauge each state’s relative performance on sound budgeting and fiscal restraint. The index consists of three metrics:

- Debt service as a percentage of tax revenue,

- State & local government employment as a percentage of the state’s population, and

- State & local government spending as a percentage of state GDP.

The index ranks each state under each metric relative to all fifty states and the District of Columbia. It then equally weights and sums each of the three metrics. Finally, it ranks the value again to produce the aggregate measure of state budget competitiveness shown in Figure 1. An increase in either the comprehensive budget competitiveness metric or the three sub-metrics represents a positive qualitative change—i.e. the state is more competitive relative to other states as the index approaches 100. In 2011, Iowa scored 79 out of 100 on the State & Local Budget Competitiveness Index. It hit a low point of 74 in 2019 and has remained there since then. With an index value of 74, Iowa ranks 25th among all states and the District of Columbia, putting it right in the middle of the pack.

Figure 1 – Iowa Government Budget Competitiveness Index

Figure 2 – Iowa Government Budget Competitiveness Index Components

Figure 2 – shows the evolution of the three components included in the Government Budget Competitiveness Index. The “Government Spending as a Percentage of GDP” index declined from 74 in 2011 to 70 in 2021. The “Government Employment as a Percentage of Population” index was 66 in 2011 and fell to 57 in 2021. The “Government Debt Service as a Percentage of Tax Revenue” index decreased slightly from 97 in 2011 to 95 in 2021.

Government Debt, Tax, and Fee Revenue

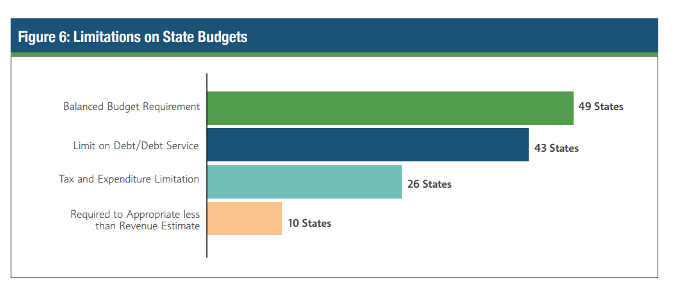

States and Local Governments may have limitations on budgets. In 2021 the National Association of State Budget Officers (NASBO) published the figures on the number of states that have limitations on state budgets by type of limit. Figure 3 shows the published figures in NASBO’s 2021 report titled, Budget Processes in the States 2021.

Forty-nine states have balanced budget amendments, forty-three have limits on debt and debt service, twenty-six have limits on tax and expenditure, and ten have appropriation limits.

Figure 3 – Limitations on State Budgets as of 2021 (Source: NASBO – Budget Processes in the States 2021)

Iowa state statute requires the governor to submit an annual budget and appropriations bills to the legislature by February 1st each year. The state has a statutory, not constitutional, requirement that the governor submit a balanced budget to the legislature and that the legislature pass and the governor sign a balanced budget. The state also has a statutory expenditure limitation, which limits General Fund expenditures at 99% of the Revenue Estimating Conference’s revenue estimate.[i] This fiscal rule effectively allows state spending to grow at the same rate as state revenue.

The state constitution prohibits the state from issuing more than $250,000 of general obligation debt without prior voter approval.[ii] In 1970, however, the Iowa Supreme Court ruled that revenue bonds are exempt from this limitation so long as they are serviced from a revenue source other than the State General Fund.[iii] In addition, Article XI, Sec. 3 of Iowa’s constitution limits local governments’ debt to 5% of the value of taxable property in its jurisdiction.

Because of the crowding out effect on the free enterprise system, CSI chose to include metrics that capture state & local governments’ revenue and debt over time to measure the amount of taxation and debt issuance from the state and local governments. The Common Sense Institute does not have data on private investment funded with debt, but data is available on public debt for state and local government from the U.S. Census, Annual Survey of State, and Local Finances. The following table shows revenue from taxes, charges, and miscellaneous revenue for state and local government in Iowa. Additionally, it shows state and local government public debt.

Table 1 shows Iowa state & local government revenue and debt. State government tax revenue increased 63.3% from $7.2 billion in 2011 to $11.8 billion in 2021. Over the same period, local government tax revenue rose 30.2% from $5.5 billion to $7.1 billion.

State Government revenue from fees (charges) and miscellaneous revenue rose 53.6% from $3.8 billion in 2011 to $5.9 billion in 2021. Local governments increased revenues from fees (charges) and miscellaneous revenue by 39.1% from $3.7 billion in 2011 to $5.1 billion in 2021.

Table 1 – Limitations on State Budgets as of 2021 (Source: NASBO – Budget Processes in the States 2021)

| Iowa State & Local Government Revenue, Debt, Spending, and GDP |

|

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

% change 2011-2021 |

| Revenue |

| State Government Tax Revenue |

$7.2B |

$7.9B |

$8.7B |

$8.6B |

$9.2B |

$9.6B |

$9.8B |

$10.1B |

$10.6B |

$10.7B |

$11.8B |

63.3% |

| Local Government Tax Revenue |

$5.5B |

$5.6B |

$5.4B |

$5.5B |

$5.6B |

$5.7B |

$5.9B |

$6.1B |

$6.4B |

$6.7B |

$7.1B |

30.2% |

| State Government Revenue from Charges & Misc. Revenue |

$3.8B |

$5.8B |

$6.2B |

$6.6B |

$7.0B |

$6.8B |

$5.3B |

$5.5B |

$5.8B |

$7.1B |

$5.9B |

53.6% |

| Local Government Revenue from Charges & Misc. Revenue |

$3.7B |

$3.7B |

$3.7B |

$3.9B |

$4.1B |

$4.3B |

$4.6B |

$4.7B |

$4.7B |

$4.9B |

$5.1B |

39.1% |

| State Government Revenue from Taxes and Charges & Misc. Revenue |

$11.1B |

$13.7B |

$14.9B |

$15.2B |

$16.2B |

$16.4B |

$15.0B |

$15.6B |

$16.4B |

$17.7B |

$17.7B |

59.9% |

| Local Government Revenue from Taxes and Charges & Misc. Revenue |

$9.2B |

$9.3B |

$9.1B |

$9.4B |

$9.7B |

$10.0B |

$10.6B |

$10.8B |

$11.1B |

$11.6B |

$12.3B |

33.8% |

| Total State and Local Revenue from Taxes and Charges & Misc. Revenue |

$20.2B |

$23.1B |

$23.9B |

$24.6B |

$26.0B |

$26.4B |

$25.6B |

$26.4B |

$27.5B |

$29.3B |

$30.0B |

48.1% |

| State Government Share Revenue from Taxes and Charges & Misc. |

54.6% |

59.6% |

62.2% |

61.8% |

62.5% |

62.0% |

58.7% |

59.1% |

59.6% |

60.5% |

59.0% |

|

| Local Government Share Revenue from Taxes and Charges & Misc. |

45.4% |

40.4% |

37.8% |

38.2% |

37.5% |

38.0% |

41.3% |

40.9% |

40.4% |

39.5% |

41.0% |

|

| Debt |

| State Government Debt Outstanding |

$7.6B |

$6.2B |

$6.7B |

$6.3B |

$6.2B |

$6.0B |

$6.1B |

$6.3B |

$6.2B |

$6.3B |

$6.4B |

-15.8% |

| Local Government Debt Outstanding |

$10.8B |

$12.0B |

$11.8B |

$12.5B |

$12.4B |

$12.6B |

$12.9B |

$12.7B |

$13.6B |

$14.2B |

$15.9B |

47.5% |

| State & Local Government Debt Outstanding |

$18.4B |

$18.2B |

$18.5B |

$18.8B |

$18.6B |

$18.5B |

$19.0B |

$18.9B |

$19.8B |

$20.5B |

$22.3B |

21.4% |

| State Government Share of Debt Outstanding |

41.2% |

34.0% |

36.1% |

33.7% |

33.5% |

32.2% |

32.3% |

33.1% |

31.3% |

30.6% |

28.6% |

|

| Local Government Share of Debt Outstanding |

58.8% |

66.0% |

63.9% |

66.3% |

66.5% |

67.8% |

67.7% |

66.9% |

68.7% |

69.4% |

71.4% |

|

| GDP |

| Iowa GDP |

$149B |

$159B |

$162B |

$173B |

$180B |

$181B |

$185B |

$192B |

$196B |

$197B |

$217B |

46.1% |

| Spending |

| State & Local Government Direct Expenditures |

$30.3B |

$31.3B |

$31.1B |

$32.5B |

$33.7B |

$34.6B |

$35.0B |

$36.1B |

$37.4B |

$40.4B |

$42.5B |

40.2% |

Over the ten years from 2011 to 2021, the growth in state government and local government revenue outpaced the growth in state GDP. Total state and local government revenue from taxes, fees, and miscellaneous revenue rose 48.1% from $20.2 billion in 2011 to $30 billion in 2021. Meanwhile, the state’s GDP increased by just 46.1% from 148.5 billion in 2011 to $231.1 billion in 2021. Note that these figures predate sweeping tax reform legislations enacted in 2022, which may allow GDP growth to outpace revenue growth in future years.

Figure 4 – Iowa Government Budget Competitiveness Index Components

Public debt issued by state and local governments increased 21.4% from $18.4 billion in 2021 to $22.3 billion in 2021. The share of public debt between state governments and local governments has changed from 41.2% state share and 58.8% local share in 2011 to 28.6% state share and 71.4% local share in 2021.

Iowa ranks 31st in the amount of public debt in 2021 among all fifty states and the District of Columbia. By comparison, California ranks 1st with $541.2B and Wyoming ranks 51st with $2 billion.

Government Debt Service as a Percentage of Tax Revenue

Debt service as a percent of tax revenue decreased from 5.0% in 2011 to 3.5% in 2021. Over the period, state debt fell by 15.8% while state revenues have increased. Despite this decrease, the competitiveness index for debt service as a percent of tax revenue has declined from 97 in 2011 to 95 in 2023. This is the result of a few states having lowered debt services as a percentage of tax revenue more than to Iowa over the same period. Iowa nonetheless remains one of the most competitive states by this metric.

The state’s constitutional debt limitations and relatively high overall tax burden likely contribute to the state’s low debt service to tax revenue ratio.[iv] The 2022 tax cuts that will be phased in through 2026 may reduce cause Iowa to fall slightly in this index metric, but it will likely improve its ranking in “government spending as a percentage of GDP.”

Figure 5 – Iowa State & Local Government Debt Service as a Percentage of Tax Revenue – Competitiveness Index and Metric

Government Employment as a Percentage of Population

The Common Sense Institute chose the percentage of state and local government employment as a percentage of the population as a measure of government encroachment. Figure 6 shows the competitive index and government employment as a percentage of the population. Iowa’s competitiveness has declined on the index from 66 in 2011 to 57 in 2023. This is the result of government employment as percentage of population increasing from 5.7% in 2011 to 5.9% in 2021.

Again, these figures come from 2021 data and do not reflect recent policy changes that may improve Iowa’s index score. Last year, Gov. Reynolds signed SF 514, reducing the number of cabinet-level state agencies from 37 to 16. This change will presumably reduce state government employment relative to the population in future years.

Figure 6 – Iowa Government Employment as a Percentage of the Population – Competitiveness Index and Metric

Government Spending as a Percentage of GDP

Between 2011 and 2023, Iowa fell from 74 to 69 in the Government Spending as a Percentage of GDP Competitive Index. Government spending as a percentage of GDP decreased from 20.4% in 2011 to 19.6% in 2021. Government spending increased by 40.2% from 2011 through 2021, which is less than the 46.1% change in GDP. Improvements in other states drove the relative decline in Iowa’s competitiveness according to this index.

Iowa ranks 22nd in the percentage change in GDP from 2011 through 2023. By comparison, Utah ranks 1st in GDP growth with 79.5% and Alaska ranks 51st with the lowest increase in GDP at 0.8%.

Iowa will likely rise in this index in future years as Governor Reynolds’ 2018 and 2022 tax reforms are fully phased in through 2026. The reforms will take Iowa from a 9-tier individual income tax structure with a top rate of 8.98% to a flat individual income tax rate of 3.9% in 2026, taking Iowa from one of the most burdensome states for individual income taxes in the nation to one of the least burdensome.

Figure 7 - Iowa Government Spending as Percentage of GDP

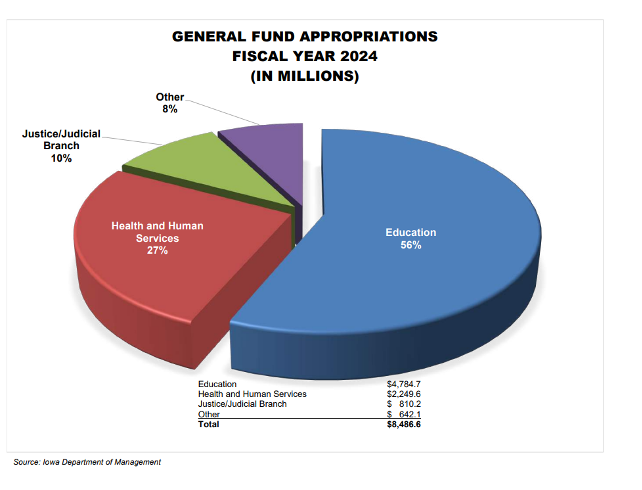

The total general fund is $8.487 billion. Figure 8 shows the largest categories of general fund appropriations for the FY 2024 state government budget. Education’s share is the largest at 56%, followed by health and human services with 27%, and the judicial branch at 10%.

By comparison, the total general fund in 2011 was 5.321 billion, education’s share was 16.2%, health and human services accounted for 24.9%, and the judicial branch garnered 12%.

Figure 8 – Iowa State Government Budget FY 2024

Going Forward

Government spending has outpaced inflation and population growth in recent years. Additionally, government employment has increased 10.3% (17,778 jobs) since 2011, more than the 4.3% increase in the population.

Failure to manage public sector spending and public sector employment growth in a fiscally responsible manner will erode Iowa’s competitiveness relative to other states. Other states that have failed to be fiscally responsible have experienced massive out-migration, reducing the tax base and putting further pressure on state and local government budgets. Clearly, Iowa has room for improvement to better compete with other states on the burden of state government spending.

Fortunately, Governor Reynolds and the legislature have pursued policies in recent years that will likely improve Iowa’s standings in these indices as the policies are fully phased in. Most notably, SF 514 reduced the number of cabinet-level state agencies from 37 to 16 and HB 2317 and other tax reform measures will significantly reduce the tax burden and thus state revenue and state spending. The former has the potential to improve Iowa’s score on the Government Employment as a Percentage of the Population Index in future years. The later has the potential to improve its score on the Government Spending as Percentage of GDP Index.

Today, Iowa is in the middle of the pack on state budget competitiveness, but there is reason to believe its standing will improve in future years.

Sources and Notes

[i] Iowa Department of Management, “Is there an expenditure limitation for the general fund?,” https://dom.iowa.gov/faq/state-budget/there-expenditure-limitation-general-fund.

[ii] State of Iowa, Legislative Services Agency, Outstanding Obligations Report, Fiscal Services Division, February 2014, https://www.legis.iowa.gov/docs/publications/SOR/861757.pdf.

[iii] Farrell v. State Board of Regents, 179 N.W.2d 533, 542-545 (Iowa 1970).

[iv] Erica York, Jared Walczak, “State and Local Tax Burdens, Calendar Year 2022, Tax Foundation https://taxfoundation.org/data/all/state/tax-burden-by-state-2022/. In 2021, the year from which CSI’s State Budget Competitiveness report pulls data, the Tax Foundation ranked Iowa as the 15th highest tax state, down from 13th highest in 2019.