SUMMARY & KEY FINDINGS

Housing affordability in the United States has remained relatively stable over time, as rising prices have been offset by lower borrowing costs. Over the last 18 months, housing affordability has begun to collapse in the face of first rapid price increases and now rapid interest rate hikes. This problem is even more acute in Arizona and the Phoenix metro market, where prices have increased much more quickly than nationally; prices here have risen 40% since the end of 2020, versus 25% for the United States[i].

- Despite relative stability over time, housing costs - as a function of both prices and interest rates - have exploded since mid-2020 since first home prices and now 30-year rates have ballooned. As measured by CSI’s ‘home buyer misery index’, housing costs in Phoenix are now double their long-run average.

- Owing partly to supply-constraints imposed given the presumption the 2006 ‘housing bubble’ was caused by speculative overbuilding, Arizona has underbuilt over the last decade, and today has a shortfall of about 95,800 housing units. A burgeoning Arizona home-construction boom may not survive a cooling US economy and housing market.

- As measured by hours of work required to service a typical 30-year mortgage, housing affordability in Arizona had been improving over time. In 1989 a typical household had to work 64 hours to make a monthly mortgage payment, versus just 41 hours last year. Since then, rising rates have increased costs in terms of time to over 65 hours, and at current prices mortgage rates rising to 8% would push costs to nearly 90 hours per month – unsustainably high.

Though not yet apparent in the (lagging) data, CSI believes rising interest rates, a slowing economy and lofty values will end Arizona’s home price appreciation and may even induce some general price declines.

HOUSING COSTS & THE HOMER BUYER MISERY INDEX

In 1989, a typical home in Arizona cost less than $100,000 – versus $445,000 today

[ii]. 30-year mortgage rates, on the other hand, have fallen over the past 30 years from 10.7% in 1989 to a low of under 2.9% by the end of 2021

[iii]. These divergent trends create a counterintuitive tendency in affordability, and accounting for both in a normalized “buyers misery index” reveals an unexpected fact: affordability was relatively stable over the past thirty years (at an index value of ~100.0). Two periods exhibit significant deviation from this trend: the “housing bubble” of the late-2000’s, and the post-2020 period of rapid increases.

- Housing costs – as a function of both prices and interest rates – had been unexpectedly stable over time. Home prices appear to have an inverse relationship with mortgage rates.

- Beginning in late-2020, home prices began accelerating rapidly, and rapid price increases continued even after mortgage rates began to rise this year. Between Aug. 2010 and Aug. 2020, the buyer misery index increased at an average rate of 0.3%/month. Since then, it has increased at an average rate of 2.3%/month – more than 7 times faster.

- Mortgage costs have begun rising rapidly, and average rates (5.81% today) have doubled in less than one year. This has serious consequences for affordability, which as measured by the buyer misery index has fallen by 29% in just 10 months. ow

- Today, home costs in the Phoenix metro market are arguably worse than they have ever been, with the buyer misery index at twice its long-run average and 31% above its prior peak in 2006. Confirming the sensitivity of home buyers to the combined costs of mortgage rates and home prices, after peaking on June 23, 30-year average rates have since fallen 9% on cooling demand.

HOUSING SUPPLY OVER TIME

Most observers agree that housing supply – and particularly the supply of affordable, accessible housing – has failed to keep up with demand both nationally and in Arizona. It appears that after a building boom in the mid-2000’s that succeeded in bringing the states per capita housing stock to its highest levels in modern state history, building slowed dramatically after 2010 and has since failed to keep pace with population growth.

- Between 2010 and 2020, the State added 243,000 new housing units but population grew by 779,000 people (3.2 people per unit)[iv]. This created a cumulative housing deficit of approximately 72,000 units ahead of the pandemic (2% of total stock).

- In 2020, a net 105,000 Americans moved to Arizona – versus about 46,000 on average over the prior 10 years. This domestic migration has fueled all the state’s recent population gains as natural growth has stalled, and these migrants would have had immediate housing needs (versus lagged needs arising from population growth driven by natural births).

- Combined with demand changes induced by pandemic response, unprecedentedly low interest rates, and large Federal cash transfers, these factors created a market shock which precipitated current prices.

- On the other hand, the state appears to be on the cusp of its largest housing construction boom in a decade. Arizona added 46,200 new housing units in 2021, and based on permits data[v], is on pace to add over 70,000 units this year.

- CSI estimates the current Arizona housing unit shortfall at approximately 95,000 units. If building trends persist as expected, this will fall to 79,100 units next year, and continue falling thereafter.

- To resolve the shortfall within 5 (10) years and after accounting for expected population growth, the state needs to add 54,300 (46,400) units annually. Based on current permit data the state is adding over 70,000 units annually.

- However, demand may already be cooling and the economy slowing. This may induce developers to curtail new construction and end our burgeoning building boom before it can close these gaps. Policymakers should pursue supply-friendly policies that enable the development of the state’s housing stock while avoiding the demand-side subsidies that put pressure on prices.

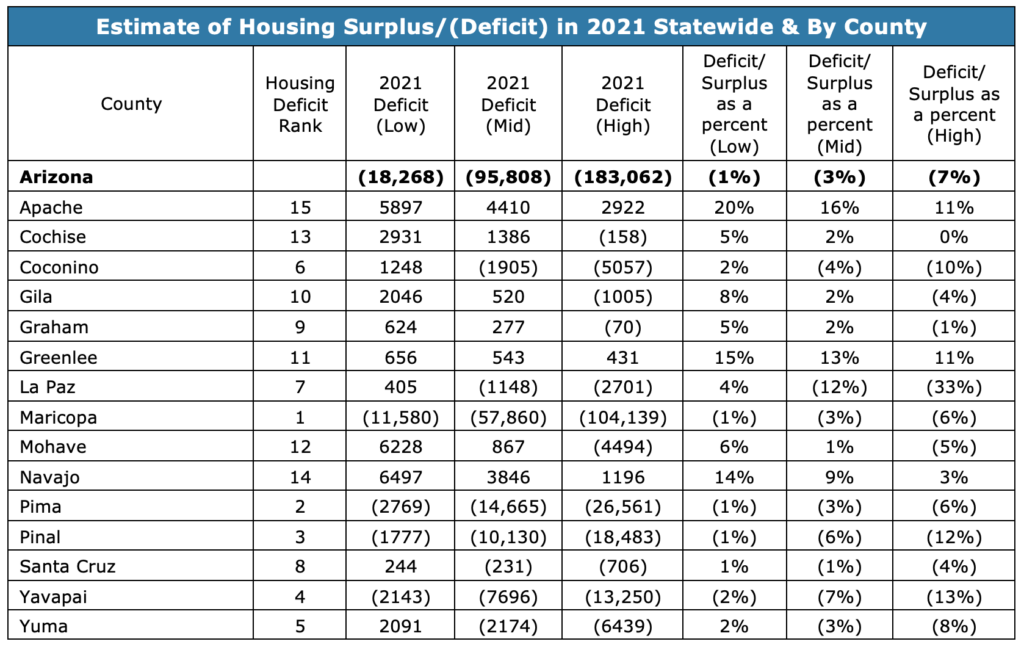

- Table 1 at the end of this report details the statewide shortfall by county. Notably, many of the state’s rural counties have housing surpluses, due to slower household formation and population growth. The bulk of the state’s shortage is concentrated in Maricopa, Pima and Pinal counties.

HOUSING AFFORDABILITY

As discussed above, the

cost of housing is not simply a function of home prices, but also interest rates. This is because approximately 90% of home purchases are financed. On the other hand, housing

affordability is a function not just of prices and interest rates but also incomes, given that relatively wealthier households are presumably better able to absorb price increases. However, simply comparing mortgage costs to household incomes may be a biased measure affordability since households can change their hours worked over time in response to norms and preferences (wage rates, dual-income households, etc.). Instead, CSI considers – at prevailing average hourly wage rates, 30-year interest rates, and home prices – how many hours a typical household would need to work to make their monthly mortgage payment. This provides a consistent basis of comparison to determine how

affordable – in terms of household hours – housing is across time and independent of other changes.

- In January 1989, at an estimated average hourly wage of $11.21, typical home price of $96,743, and an average 30-year mortgage rate of 10.73%, an Arizona household would need to work for 64 hours to make their monthly mortgage payment. This fell to a pre-bubble low of under 43 hours in mid-2003.

- By the peak of the housing bubble in mid-2006, housing affordability reached its lowest CSI-recorded levels - with the typical household having to work over 77 hours to make their monthly payments. This then fell to an all-time low of just 23 hours by January 2012.

- As recently as mid-2021, Arizona households would have had to work 43 hours/month to service mortgage costs at (gross) prevailing wages of $29.84 - effectively returning affordability to levels seen in the early 2000’s and well below levels in 1989.

- Since then, affordability has collapsed as costs have risen rapidly and hourly earnings growth has slowed. As of May 2022, households must work nearly 66 hours to service a typical monthly mortgage - a 64% increase in just one year.

- Strikingly, however, in terms of workhours required to meet monthly mortgage costs, housing remains more affordable today than it was in mid-2006.

- Rising mortgage costs will destroy affordability at current prices. If typical home prices in the Phoenix metro market remains at about $450,000 and mortgage rates rise to 8.0%, a household would need to work nearly 90 hours to service a monthly mortgage payment - a rate without historical precedent and over half the expected workhours of a typical worker.

- These kinds of levels are simply not sustainable – it would take a change in interest rates and/or hourly incomes relative to current trends to maintain housing demand at current price levels. If neither of those can adjust, then it seems almost certain that price levels will fall, and demand will cool – an outcome perhaps favored by home buyers but not by homeowners.

© 2022 Common Sense Institute

[i] S&P Dow Jones Indices LLC, S&P/Case-Shiller U.S. National Home Price Index [CSUSHPINSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CSUSHPINSA, July 11, 2022.

[ii] Zillow, Zillow Home Value Index; https://www.zillow.com/research/data/, July 11, 2022.

[iii] Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, July 11, 2022.

[iv] U.S. Census Bureau, Estimates of Housing Units & Population; https://www2.census.gov/programs-surveys/popest/tables/, July 11, 2022.

[v] U.S. Census Bureau, New Private Housing Units Authorized by Building Permits for Arizona [AZBPPRIVSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/AZBPPRIVSA, July 11, 2022.